Suriname emerges as a high-potential offshore E&P frontier

Key Highlights

- Suriname's offshore sector is transitioning from exploration to development, with the GranMorgu project marking its first deepwater commercial milestone.

- Major operators like TotalEnergies, APA, Shell, and Petronas are actively drilling, appraising, and developing discoveries across multiple blocks, with a focus on deepwater plays.

- Suriname’s licensing and local content initiatives, along with infrastructure expansion, are preparing the country for a significant offshore production future, potentially reaching 200,000+ barrels per day by 2030.

Suriname has emerged as a high-potential but still-maturing offshore E&P frontier within the Guyana-Suriname Basin, sharing the same prolific petroleum system that powers Guyana’s success.

While it lags Guyana in production scale, recent discoveries, the FID on the country’s first major deepwater development, and ongoing licensing have positioned it for significant growth. As of mid-2026, Suriname remains exploration-heavy with one flagship development advancing toward first oil in 2028.

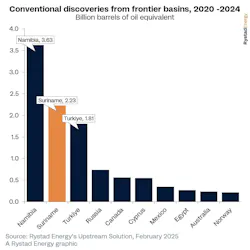

Over the past two to three years, Suriname has transitioned from promising frontier discoveries to concrete development commitments. Exploration in Block 58, operated by TotalEnergies (50%) with APA Corporation (50%), yielded key finds such as Sapakara South (2021) and Krabdagu (2022). These, along with earlier hits like Maka Central and Kwaskwasi, confirmed substantial resources. By 2023–2024, appraisal drilling solidified the commercial case, with recoverable volumes for the initial phase estimated at around 700–760 million barrels.

Seismic activity ramped up during this period, with multi-client 3D surveys enhancing imaging of Cretaceous turbidite plays across shallow and deepwater areas. Operators including Shell, Chevron, TotalEnergies, QatarEnergy, and Petronas pursued additional drilling in blocks like 52, 53, and others, delivering a mix of oil, gas, and condensate finds—though success rates reflected the inherent risks of frontier basins.

Field development gained momentum in 2023–2024 as partners advanced FEED studies for Block 58. In October 2024, TotalEnergies and APA reached FID on the GranMorgu project (encompassing the Sapakara South and Krabdagu fields), committing approximately $10.5 billion. This marked Suriname’s first deepwater commercial development. Staatsolie exercised its option for up to a 20% participating interest. No offshore production existed yet—onshore output from Staatsolie’s mature heavy oil fields hovered around 17,000 barrels per day—but planning for infrastructure accelerated.

Contracts flowed quickly post-FID. SBM Offshore, in partnership with Technip Energies, secured the FPSO contract using a Fast4Ward-style hull. Saipem won the $1.9-billion subsea scope. The design features an all-electric FPSO with 220,000 barrels per day capacity, gas reinjection for low emissions (targeting minimal flaring), and provisions for future tiebacks.

The government, through Staatsolie, supported this progress with licensing initiatives. Shallow Offshore Round 2 and other efforts awarded blocks, while production-sharing contracts emphasized exploration commitments and Staatsolie back-in rights. Fiscal terms remained competitive to draw international capital into the basin’s Guyana analogs.

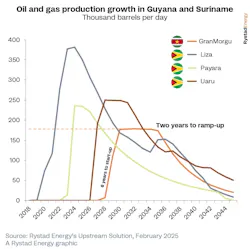

As of mid-2026, GranMorgu stands as the centerpiece of Suriname’s offshore ambitions. Post-FID execution is advancing steadily, with overall project progress exceeding 30% in some updates and FPSO construction around 60%. Development drilling is scheduled to commence in late 2026 or Q1 2027, involving up to 32 wells (including producers and injectors). Subsea fabrication, flowlines, and installation activities are ramping up, all aligned with a 2028 first-oil target.

Exploration continues in parallel, though results have been mixed. In Block 52, Petronas (operator) declared commerciality for the Sloanea gas discovery in late 2025, with additional oil finds at Roystonea and Fusaea under evaluation. A potential FID for gas developments could come in 2026, targeting first gas around 2030 via FLNG or similar solutions. Other operators like Shell, Chevron, and TotalEnergies (which added a stake in Block 53) have drilled or planned high-impact wells, testing deeper plays amid roughly 10 offshore wells anticipated across 2025–2027.

Seismic coverage has improved, with about 50% of the basin now licensed and holding modern 3D data. Onshore production remains the sole source of current output, but logistics bases, local content programs (aiming for over $1 billion in spend), and supply chain buildup are preparing for offshore operations.

Looking ahead to 2026–2029, Suriname is poised for its first offshore oil production. GranMorgu’s ramp-up in 2028 could deliver peak rates near 220,000 barrels per day, providing a major economic boost through revenues, jobs, and GDP growth. Tieback opportunities may extend the plateau, while successful appraisal could unlock cluster developments.

Exploration momentum is expected to persist, with further wells targeting extensions and new plays. Block 52’s gas commercialization, if sanctioned, would diversify the portfolio and potentially introduce LNG elements. Staatsolie’s Open-Door Offering, launched in November 2025, keeps momentum alive: it covers roughly 60% of offshore acreage (over 70,000 km²) across shallow to ultra-deep waters. Companies can nominate blocks, propose work programs, and choose flexible arrangements like PSCs, joint studies, or technical evaluations. A Houston roadshow in May 2026 highlighted this to attract new entrants.

Production forecasts suggest that Suriname could reach low hundreds of thousands of barrels per day (including onshore) by the early 2030s if additional FIDs materialize. Infrastructure will expand with dedicated logistics hubs in Paramaribo and enhanced local capabilities.

Challenges remain, including geological risks in frontier plays, execution complexities in deepwater, commodity price volatility, and the need for robust local content and environmental management. Yet the proven petroleum system, improving data, competitive terms, and low-emission project designs provide strong tailwinds.

Suriname stands at a pivotal inflection point. From exploration successes in the early 2020s to the GranMorgu development now under construction, the country is steadily converting potential into reality. The next two to three years will be defining—marked by the start of development drilling, potential new sanctions, and the dawn of offshore production in 2028. If execution stays on track and exploration delivers, Suriname could follow a scaled version of Guyana’s transformative path, cementing its role as a notable player on the Atlantic margin.

About the Author

Bruce Beaubouef

Managing Editor

Bruce Beaubouef is Managing Editor for Offshore magazine. In that capacity, he plans and oversees content for the magazine; writes features on technologies and trends for the magazine; writes news updates for the website; creates and moderates topical webinars; and creates videos that focus on offshore oil and gas and renewable energies. Beaubouef has been in the oil and gas trade media for 25 years, starting out as Editor of Hart’s Pipeline Digest in 1998. From there, he went on to serve as Associate Editor for Pipe Line and Gas Industry for Gulf Publishing for four years before rejoining Hart Publications as Editor of PipeLine and Gas Technology in 2003. He joined Offshore magazine as Managing Editor in 2010, at that time owned by PennWell Corp. Beaubouef earned his Ph.D. at the University of Houston in 1997, and his dissertation was published in book form by Texas A&M University Press in September 2007 as The Strategic Petroleum Reserve: U.S. Energy Security and Oil Politics, 1975-2005.