Top 5 projects to watch: Operators advance offshore field development plans

Key Highlights

- A strong emphasis on gas development, deepwater platforms, and low-emissions technologies underscores the industry’s pivot toward cleaner, more efficient offshore energy solutions in 2026.

- Emerging basins in Africa and Asia-Pacific dominate the project list, reflecting strategic moves by IOCs and NOCs to capitalize on resource potential and regional energy security needs.

- Infrastructure investments are substantial, with newbuild FPSOs, subsea systems, and cross-border LNG facilities driving high capital expenditure and engineering complexity.

By Bruce Beaubouef, Managing Editor

Buoyed by high prices and rising energy demand, offshore operators and international oil companies are advancing plans for several field development projects, and 2026 looks to be a busy year for offshore construction activities.

With that in mind, the editors of Offshore have compiled the following Top 5 field development projects to keep an eye on this year.

The projects are:

- Venus project offshore Namibia,

- Rovuma LNG project offshore Mozambique,

- Longtail project offshore Guyana,

- GTA Phase 2 offshore Mauritania and Senegal, and

- Geng North offshore Indonesia.

The projects were selected primarily on the basis of an expected or upcoming FID, but other parameters included notable aspects such as size of reserves; infrastructure scale and scope; unique milestones such as first deepwater production; regional milestones; or low-emissions designs or emissions reductions technologies.

These projects highlight a mix of emerging basins, gas-focused transitions, and innovative low-emissions approaches amid evolving global energy dynamics. Timelines are subject to final regulatory approvals, partner alignments, and external factors.

Below, we examine each of these projects in detail to determine how they became “the projects to watch” in 2026.

Venus

The Venus project, operated by TotalEnergies in Namibia’s Orange basin, stands out as one of the most anticipated offshore developments in Africa. Phase 1 targets approximately $5 to $10 billion in capex, with recoverable resources estimated at 750 million barrels of oil equivalent (MMboe) for the initial phase and total field potential up to 5.1 billion barrels. Infrastructure includes a deepwater FPSO with a capacity of around 160,000 barrels per day, subsea tiebacks, and potential for a multi-FPSO hub integrating nearby discoveries such as Mopane.

This project marks Namibia’s first FPSO development and a major milestone as Africa’s sub-Saharan entry into large-scale deepwater production (water depths around 3,000 meters). A key highlight is its low-emissions design, aiming for an intensity below 15 kg CO2e/boe through full electric architecture, closed flares, and vapor recovery units. TotalEnergies and partners are actively working toward FID in mid-2026, with first oil targeted for 2030.

Rovuma LNG

ExxonMobil’s Rovuma LNG project in Mozambique’s Area 4 represents a massive revival of the country’s LNG ambitions following security-related delays. Total capex is estimated at $24 to $30 billion, drawing from reserves of 15-20 trillion cubic feet (Tcf) in Area 4 (part of the basin’s overall ~75 Tcf). The scope features offshore subsea systems and pipelines feeding into onshore modular LNG trains with 18 million tonnes per annum capacity, plus shared facilities with adjacent developments. This integrated approach supports low-GHG modular e-LNG design to reduce emissions and risks.

While exact figures are not public, the total offshore upstream portion (including drilling, subsea systems, pipelines, and associated costs) is likely in the $7 to $12 billion range based on similar integrated LNG projects.

The offshore components include drilling 60 subsea wells at $6 to $7 billion. Each deepwater well is expected to cost $100 to $120 million, including appraisal and completion, phased over 5 to 10 years.

Subsea, equipment will include subsea production systems, manifolds, umbilicals, and boosting pumps at an approximate overall cost of $2 to $3 billion, including fabrication and installation. An additional $1 to $2 billion will be spent on pipelines and risers, to be placed in a 45-km corridor. These will be multiple relatively large-diameter lines, with installation via reel-lay vessels. Another $1 to $2 billion is expected to be spent on surveys and tie-ins.

Total offshore spend is expected to comprise 30% to 40% of the total $24 to $30-billion project capex, but the offshore upstream components are the project enabler. The onshore LNG trains (12 modular units) dominate the remaining spend (~$15 to $20 billion), but FID hinges on offshore viability.

The project is poised to mark Mozambique’s return as a top global LNG exporter. Front-end engineering and design (FEED) is advancing, with FID expected within the first half of 2026, and first LNG around 2030.

Longtail

ExxonMobil’s Longtail development in Guyana’s Stabroek Block introduces a significant shift toward non-associated gas production. Capex is around $12.5 billion, focusing on substantial gas volumes plus ~250,000 barrels per day of condensate capacity. The core infrastructure is a newbuild FPSO tailored for gas and condensate handling, with subsea systems.

ExxonMobil is reportedly planning a super-sized FPSO for the Longtail project, with environmental authorization sought for a unit expected to be larger than previous developments. The new Longtail FPSO vessel is expected to be part of the next wave of projects aimed at boosting Guyana’s production, joining a fleet of vessels that currently feature high-capacity oil storage (typically two million barrels) and high-volume water injection.

As Guyana’s first dedicated non-associated gas project, the Longtail project supports its national gas-to-energy goals, industrial growth, and reduced flaring. While building on the mature Stabroek basin’s efficiencies, it brings novelty through this gas-priority pivot amid rising global demand. ExxonMobil plans to submit the field development plan soon, targeting regulatory approvals and FID by end-2026, with startup around 2030.

GTA Phase 2

bp’s Greater Tortue Ahmeyim Phase 2 expands the pioneering cross-border gas project between Mauritania and Senegal. Capex is estimated at $3 to $5 billion, building on the Tortue field’s ~15 Tcf reserves. Infrastructure centers on a gravity-based structure for 2.5-3 million tonnes per annum of LNG, with additional subsea tiebacks to Phase 1’s FPSO and FLNG facilities for shared operations.

GTA Phase 2 represents West Africa’s first cross-border deepwater gas expansion, promoting regional LNG growth and energy security in the Sahel region. It incorporates low-carbon features from the initial phase, such as combined-cycle power. FID remains pending but targeted for 2026, with construction potentially starting in 2028 and first gas around 2030.

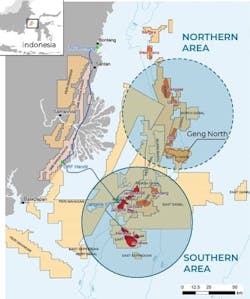

Geng North

Eni’s Geng North project (part of the Northern Hub development) in Indonesia’s Kutei basin is advancing rapidly toward sanction. Capex is estimated at around $15 billion (combined with related fields like Gendalo-Gendang), targeting reserves of approximately 5 Tcf of gas and 400 million barrels of condensates from Geng North alone, plus additional volumes from integrated discoveries (e.g., Gehem ~1.6 Tcf) for overall production of ~2 Bcf/d of gas and 80,000 b/d of condensates.

New infrastructure will be centered on a newbuild FPSO (handling ~1 Bcf/d gas + 80,000 b/d condensates, with 1MM bbl of storage), subsea wells, flowlines, onboard gas treatment, and pipelines to onshore facilities (Santan Terminal/Bontang LNG for partial export/domestic use), with condensates transported via shuttle tankers.

This project is expected to create a new production hub in the basin, and serve as a model for future Indonesian gas developments that support both domestic supply and international markets. Indonesia’s regulator SKK Migas expects FID in March 2026 (following 2024 POD approvals), with first production targeted for late 2027.

Common drivers

The Top 5 projects selected share several strong common drivers that reflect broader upstream trends in offshore E&P developments. These include a heavy focus on natural gas development, ultra-deepwater plays with associated floating platform components, the move to frontier or emerging offshore areas, and emissions reduction technologies or efficiency features. These trends are examined below.

Four of the Top 5 are fundamentally gas-focused or gas-dominant:

- Rovuma LNG: Pure LNG revival play with massive onshore trains fed by offshore subsea gas.

- Geng North: Deepwater gas hub (~5 Tcf+ in Geng North alone, feeding Bontang LNG and domestic supply).

- GTA Phase 2: Cross-border gas expansion tied to LNG output via gravity-based structure.

- Longtail: Guyana’s first dedicated non-associated gas/condensate project, shifting Stabroek toward balanced oil-gas.

Even Venus, which is primarily oil, has significant associated gas potential in a basin where gas monetization discussions are emerging. This mirrors the 2026 global trend: gas/LNG projects are driving many FIDs amid rising Asian/European demand, energy security needs, and LNG export opportunities—while pure oil greenfields face softer momentum due to price outlooks and transition pressures.

All five projects call for significant offshore infrastructure, often with newbuild or expanded platforms/FPSOs that drive high capex:

- Venus: Deepwater FPSO (potential multi-FPSO hub)

- Longtail: Newbuild FPSO for gas/condensate

- Geng North: Newbuild FPSO with onboard gas treatment (~1 Bcf/d capacity)

- GTA Phase 2: Gravity-based structure plus subsea tiebacks to Phase 1 FPSO/FLNG

- Rovuma: Offshore subsea/pipelines feeding onshore LNG (upstream offshore elements).

These trends tie into the broader 2026 surge in offshore FIDs (especially deepwater), where platforms enable scale, efficiency, and access to large reserves in mature or emerging basins. These projects are hub-scale developments with substantial engineering and fabrication needs.

Each of the projects are located in emerging areas or frontier basins, with a particular focus on the global south:

- Venus: Namibia’s Orange basin (Africa’s new frontier hotspot)

- Rovuma: Mozambique’s Rovuma basin (reviving post-insurgency)

- GTA Phase 2: Mauritania/Senegal border (West Africa’s cross-border pioneer)

- Geng North: Indonesia’s Kutei basin (deepwater gas hub model)

- ongtail: Guyana’s Stabroek (mature but still expanding fast).

The list leans heavily toward Africa (three projects) and Asia-Pacific (one), with Guyana as a South American outlier. This reflects 2026 patterns: emerging basins in Africa (Namibia, Mozambique, Mauritania/Senegal) and Asia-Pacific (Indonesia) are seeing renewed interest for large gas/oil finds, often with IOCs (TotalEnergies, Exxon, Eni, bp) leading alongside NOCs or governments. These regions offer lower-cost opportunities, resource nationalism incentives, and alignment with global LNG/gas demand.

A few of the projects include low emissions or efficiency features. Venus has explicit low-emissions designs (<15 kg CO₂e/boe, electric architecture, closed flares), while others have modular or efficient designs (Rovuma e-LNG, GTA low-carbon carry-over); efficient FPSOs (Longtail/Geng North); or gas utilization to reduce flaring (Longtail).

While not universal, emissions reduction or efficiency tech appears as a differentiator—helping secure approvals, partners, and buyers in a world with tightening regulations and ESG scrutiny.

Overall, these projects capture the 2026 offshore upstream “sweet spot”: gas-heavy, deepwater/platform-driven projects in emerging African/Asian basins that prioritize monetization (LNG/export/domestic), efficiency, and some decarbonization edge. They represent the industry’s pivot toward reliable, large-scale gas supply amid energy transition pressures, while still delivering big reserves and capex impact.

Honorable mentions

There are a number of offshore upstream oil and gas projects that were set to reach FID this year, or in fact had reached it, that were strong contenders for the Top 5. But these were excluded due to higher uncertainty around timelines, ongoing delays, geopolitical/ security risks, or other factors. These projects still carry significant capex, reserves, infrastructure scale, and other unique aspects, making them worth monitoring closely.

Leviathan expansion

Chevron’s Leviathan expansion (Phase 1B) in Israel’s Leviathan field targets incremental capex of approximately $2.3 to $2.4 billion, building on the field’s existing ~22 tcf recoverable gas reserves. The project involves drilling three additional offshore wells, adding subsea infrastructure, and upgrading treatment facilities on the existing fixed production platform to boost total output to around 21 billion cubic meters per annum (Bcm/year). It supports regional energy security through increased supplies to Israel, Egypt, and Jordan under long-term export agreements.

The expansion would enhance efficient gas utilization and tie into Eastern Mediterranean export hubs. Chevron and partners (NewMed Energy, Ratio Energies) took FID in January 2026, with startup targeted toward the end of the decade. However, recent security concerns led to a temporary production shutdown and force majeure declaration in early March 2026 amid regional hostilities, introducing execution risks and potential delays despite the earlier sanction.

Cá Voi Xanh (Blue Whale)

ExxonMobil’s Cá Voi Xanh (Blue Whale) project in Vietnam’s Block 118 remains a high-potential but uncertain contender. Capex estimates range from $10 to $12 billion, based on reserves of approximately 5 trillion cubic feet of natural gas. The development includes a fixed offshore platform, subsea pipelines, and onshore gas treatment facilities to supply around 3 GW of power generation via integrated gas-to-power chains. As Vietnam’s largest gas field, it offers a milestone for deepwater production in contested waters and supports energy security through efficient pipeline transport. Progress has been slow due to regulatory and geopolitical factors, with ongoing pushes for acceleration per contract terms. FID could occur in 2026-2027 if commercial agreements advance, with first gas potentially 2027-2028 (though delays remain possible).

Zama

The Zama oil field, now operated by Harbour Energy (with partners Pemex, Talos Energy Mexico, and Grupo Carso), is a major shallow-water discovery with significant recoverable resources (estimated hundreds of millions of barrels of oil). Capex would likely fall in the multibillion-dollar range for full development, involving fixed platforms, subsea systems, and tiebacks in the Bay of Campeche. As one of Mexico’s largest recent discoveries, it represents a milestone for post-reform shallow-water development and shared-reservoir cooperation. Engineering and design work is targeted for completion in 2026, paving the way for FID thereafter (potentially late 2026 or into 2027), with first production delayed accordingly. Operator transition and ongoing partner alignment have contributed to timeline extensions from earlier expectations.

Cronos

Eni (50%, operator) and TotalEnergies (50%) are advancing the Cronos gas field in Cyprus’ Exclusive Economic Zone, with estimated gas in place of 3.1–3.4 trillion cubic feet (Tcf). The proposed infrastructure consists of subsea production systems (wells, manifolds, flowlines, and tiebacks) connected via a ~90 km subsea pipeline to Egypt’s existing Zohr field facilities for processing, followed by export through the Damietta LNG terminal. No new major platforms or onshore LNG trains are planned, as the project relies instead on a subsea tieback to under-utilized Egyptian infrastructure for cost efficiency and faster timelines. FID is targeted for 1Q 2026 (potentially by end-March or early 2Q), with first gas eyed for late 2027 or 1H 2028. For Cyprus, Cronos represents a potential milestone as the country’s first commercial production from its EEZ discoveries, while reinforcing Egypt’s role as a regional gas hub and contributing to European energy security through additional LNG supply.

These honorable mentions illustrate the fluid nature of upstream FID timelines—strong fundamentals can be offset by external risks like security (Leviathan), negotiations/ regulatory hurdles (Cá Voi Xanh), or operator/partner dynamics (Zama). One or more of these projects could reach FID any time this year, and even move into construction. They too are worth keeping an eye on.

About the Author

Bruce Beaubouef

Senior Lead Reporter / Managing Editor

Bruce Beaubouef is Managing Editor for Offshore magazine. In that capacity, he plans and oversees content for the magazine; writes features on technologies and trends for the magazine; writes news updates for the website; creates and moderates topical webinars; and creates videos that focus on offshore oil and gas and renewable energies. Beaubouef has been in the oil and gas trade media for 25 years, starting out as Editor of Hart’s Pipeline Digest in 1998. From there, he went on to serve as Associate Editor for Pipe Line and Gas Industry for Gulf Publishing for four years before rejoining Hart Publications as Editor of PipeLine and Gas Technology in 2003. He joined Offshore magazine as Managing Editor in 2010, at that time owned by PennWell Corp. Beaubouef earned his Ph.D. at the University of Houston in 1997, and his dissertation was published in book form by Texas A&M University Press in September 2007 as The Strategic Petroleum Reserve: U.S. Energy Security and Oil Politics, 1975-2005.