Offshore vessel fleets tighten amid sustained supply discipline

Key takeaways:

- The global offshore support vessel fleet is aging, with over half of the operational fleet exceeding 15 years, yet demand-driven utilization is improving due to limited reactivation and newbuilds.

- Offshore service vessels, including pipelay, ROV support and saturation dive vessels, are experiencing high utilization levels, driven by ongoing offshore projects and wind development, with limited newbuild activity constraining capacity.

- The market is moving toward utilization optimization, fleet renewal and strategic positioning, as macroeconomic risks persist but fundamental supply-demand dynamics tighten.

By Chen Wei, Westwood Global Energy Group

Across offshore energy markets, vessel fundamentals are entering a more nuanced phase of recovery. While macroeconomic and geopolitical forces continue to weigh on oil prices and capital allocation, utilization trends across offshore support, wind and service fleets point to a tightening supply-demand balance through 2026 and beyond. Fleet aging, constrained reactivation and selective newbuild ordering are increasingly shaping utilization outcomes rather than demand growth alone.

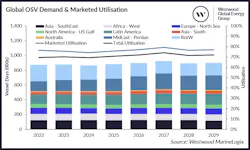

Offshore support vessels: Maturing fleet, improving balance

The global offshore support vessel (OSV) market posted modest but meaningful improvement in 2025. Demand days increased by 2% year over year, lifting marketed utilization to an average of 76%. These figures underscore a steadily tightening market, particularly when viewed against the backdrop of a maturing fleet.

More than half of the operational OSV fleet is now over 15 years old. Nevertheless, the operational fleet expanded slightly in late 2025 to 3,209 units due to newbuild deliveries, while the laid-up fleet declined marginally.

The net reactivation of only two vessels highlights a key theme: utilization is improving not because of aggressive reactivation or scrapping cycles, but because accessible and commercially viable supply is increasingly limited.

Regionally, demand remains concentrated in the Middle East, Latin America and Southeast Asia, together accounting for close to half of global OSV demand days. Operational fleet movements have been uneven. South Asia and West Africa recorded net inflows of active tonnage, while the North Sea saw the largest outflow, reflecting both regulatory pressure and continued redeployment.

The laid-up fleet has fallen sharply from more than 1,500 vessels during the COVID-19 downturn to fewer than 400 units by fourth-quarter 2025. However, demolition activity remains muted, constrained by low scrap steel prices and uncertainty around future utilization. This has preserved optionality within the supply side but at the cost of higher average fleet age.

Looking ahead, marketed utilization is forecast to rise to 77% in 2026 and exceed 79% in 2027. With the OSV orderbook standing at 216 vessels—mostly AHTS vessels and PSVs—incremental supply growth remains manageable. In essence, incremental demand growth is translating more directly into utilization upside than at any point in the past decade.

Offshore wind vessels: Capacity constraints emerge

Major offshore wind markets across the UK, Europe and APAC (excluding Mainland China) are increasingly aligning and streamlining policy frameworks to support project execution, in contrast to the US where regulatory uncertainty continues to weigh on market momentum.

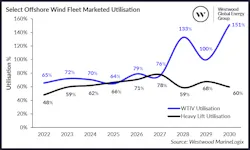

Marketed utilization for wind turbine installation vessels (WTIVs) engaged in transport and installation (T&I) activities moderated to 64% by year-end 2025, down from 70% in 2024, before rebounding to c.79% in 2026.

This acceleration is primarily driven by a step-up in turbine and foundation installation activity. Installation volumes in 2026 are expected to nearly double year over year, while cumulative installed offshore wind capacity is forecast to exceed 236 GW by 2030. Although the near-term project pipeline has softened marginally, the medium to long-term outlook remains structurally robust, underpinned by continued capacity expansion and policy support.

In 2025, a greater share of heavy-lift vessel activity was driven by offshore wind projects relative to 2024. Looking ahead, demand is expected to be supported by a resurgence in oil and gas workscopes, with utilization projected to reach about 78%.

Fleet fundamentals reinforce this utilization outlook. At the end of 2025, the global operational fleet (excluding Mainland China) comprised 38 WTIVs, 51 heavy-lift vessels, and 87 commissioning service operation vessels (CSOVs). The WTIV and heavy-lift orderbook remains limited with only five WTIVs and seven heavy-lifts on order respectively, whereas the CSOV segment is experiencing a pronounced build cycle with 58 firm orders.

Over the medium term, the WTIV T&I segment is expected to remain structurally undersupplied based on the currently visible fleet, with the heavy-lift market also showing signs of tightening. While some incremental capacity may be unlocked through the retrofitting of Mainland China units or the redeployment of vessels from the oil and gas sector, such measures are expected to provide only limited relief and remain dependent on vessel suitability and regulatory compliance.

Offshore service vessels: Selective supply tightness

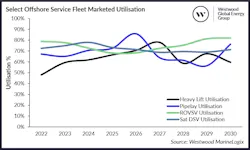

In 2025, marketed utilization averaged 73% for pipelay vessels, while ROV support vessels (ROVSVs) and saturation dive support vessels (Sat DSVs) recorded 75% and 73%, respectively.

These segments have exhibited disciplined fleet expansion, with newbuild activity remaining constrained due to the significant capital intensity required. The current operational fleet comprises 105 pipelay vessels, 207 ROVSVs and 74 Sat DSVs.

Orderbook visibility is limited across most segments, with the exception of ROVSVs, and only a single pipelay vessel is currently under construction.

ROVSVs and Sat DSVs are expected to sustain elevated utilization levels, underpinned by ongoing brownfield activity; inspection, repair and maintenance requirements; and continued offshore wind development. The inherent versatility of ROVSVs enables deployment across offshore wind workscopes, including cable installation support and walk-to-work accommodation. Demand for Sat DSVs is expected to be further supported by project activity in the Gulf Cooperation Council region and across Asia.

While the Middle East and Asia continue to account for the majority of pipelay activity, 2026 is expected to see increased contributions from regions such as Africa, Latin America and Australia, driving utilization up to about 86%.

A converging theme: Utilization optimization and strategic positioning

While macroeconomic risks persist, particularly around price volatility and policy uncertainty, underlying vessel markets are increasingly characterized by tightening fundamentals.

For owners and investors, the next phase of the cycle is expected to be defined less by rapid fleet expansion and more by optimizing utilization, advancing fleet renewal, diversifying geographically and strategically positioning for structurally tighter market conditions through the latter half of the decade.

Want more content like this?

Visit Offshore's Vessels section for daily news, project updates and technology trends.

About the Author

Chen Wei

Chen Wei is Westwood Global Energy Group's senior manager within the Offshore Energy Services team, where he manages the offshore marine function following the launch of the MarineLogix market intelligence solution. As part of the company's consulting services, he brings extensive experience across commercial studies, asset benchmarking, and strategic advisory projects, working with a diverse client base that includes vessel contractors, offshore construction companies and E&Ps.

Wei also served in a corporate strategy role at a Fortune 500 company, where he translated long‑term strategic plans into actionable commercial and operational objectives.