Declining Gulf rig counts mask rising efficiency

Key highlights:

- Rig counts in the Gulf of Mexico have decreased from over 100 in 2000 to approximately 11 in 2026, reflecting industry consolidation and technological efficiency.

- Advances such as directional drilling, high-pressure equipment, and automation have enabled fewer rigs to achieve higher productivity and maintain steady oil output.

- The shift from shallow-water to deepwater operations has resulted in fewer but larger and more capable rigs, supporting sustained or increased production despite declining rig numbers.

Bruce Beaubouef, Managing Editor

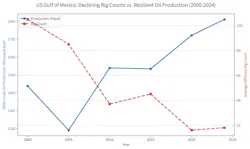

Since the turn of the century, there have been two major and seemingly contradictory oil and gas trends in the US Gulf of Mexico (GoM): declining rig counts and (more or less) growing production.

The US GoM rig count (active offshore rotary rigs, per Baker Hughes data) has shown a long-term declining trend since around 2000, with significant volatility driven by oil prices, major events (e.g., Deepwater Horizon in 2010, 2014-2016 price crash), and the shift toward onshore shale plays.

Meanwhile, US GoM (federal offshore) crude oil production has held remarkably steady or grown modestly. It averaged roughly 1.8 million barrels per day (b/d) in 2024 and climbed toward 1.9 million b/d in 2025, with forecasts for similar or slightly higher levels into 2026 as new deepwater projects (such as subsea tiebacks and new floating production units) offset natural declines from older fields. This represents a net increase from early-2000s levels despite far fewer active rigs.

The years since 2000 can be placed in the following categories:

- Early 2000s: Rig counts were relatively high, often in the 100-130 range (peaking near 122 in early 2000), with a mix of shallow-water and emerging deepwater activity.

- Mid-2000s to 2014: Fluctuated but generally trended lower as activity moved to deeper waters (requiring fewer but more capable rigs) and natural gas prospects became less economic due to onshore shale gas boom. Counts dropped to around 40-60 by the early 2010s.

- Post-2010 (Deepwater Horizon moratorium): Sharp temporary drop to ~19 in mid-2010, then recovery to ~50-60 by 2014.

- 2015-2020: Massive decline due to the oil price crash — falling to teens/low-20s, with a COVID-era low around 10-15.

- 2020s to present (as of early 2026): Stabilized in the low teens to upper teens, reflecting a mature, capital-constrained deepwater focus with fewer rigs needed for high-efficiency projects. No major rebound to pre-2010 levels.

The past 25 years have seen overall declining numbers, from triple digits to now consistently in the teens.

Average annual rig counts

The rig counts below are derived from Baker Hughes offshore rotary rigs data, EIA reports, and other industry sources:

• 2000: ~100-110

• 2005: ~80-90

• 2010: ~35-40 (post-moratorium low)

• 2014: ~50-60 (pre-crash peak in recovery)

• 2015: ~40-50

• 2016: ~20-25

• 2017: ~18-22

• 2018: ~20-25

• 2019: ~22-25

• 2020: ~15-18 (COVID-19 impact)

• 2021: ~14-17

• 2022: ~15-18

• 2023: ~16-19

• 2024: ~17-20

• 2025: ~16-19 (averages through late 2025).

For the past 10 years (2016-2025), averages have hovered in the 15-20 range, a sharp drop from the 40-plus seen in the early 2010s and far below the 100-plus of the early 2000s. As of the week of April 24, 2026, the US offshore rig count (largely Gulf of Mexico) stood at approximately 11 rigs, according to the latest Baker Hughes data — firmly in the low-teens range that has characterized much of the 2020s.

The decline reflects consolidation in the GoM — fewer, larger deepwater projects with advanced semisubmersibles and drillships, plus competition from onshore shale for capital.

The decline in the US GoM rig count has been steep and striking — dropping from triple-digit levels to consistently in the teens over the past couple of decades.

This trend highlights the GoM’s shift from high-volume shallow-water drilling to a smaller number of high-capex, high-tech deep/ultra-deep projects — fewer rigs, but often more productive ones.

Thus, the precipitous decline in the US GoM rig count since 2000 is not (just) a story of reduced activity. It is also a story of transformation, where technological advances have made rigs far more capable and efficient, meaning fewer are needed to achieve similar or even greater production levels.

This rig “transformation,” in turn, combines with other structural, economic, and regulatory factors to explain the drop from over 100 active rigs in the early 2000s to the teens today.

The core shift

In the early 2000s, the GoM was dominated by shallow-water (shelf) operations—typically in water depths under 500 feet—where drilling was relatively straightforward, lower-cost, and involved many jackup rigs targeting smaller, more numerous reservoirs. This era saw rig counts peaking around 120-150, as operators drilled a high volume of simpler wells.

However, as shallow-water fields matured and discoveries dwindled (with an 82% decline in shelf drilling over the last two decades), the industry pivoted to deepwater (1,000-5,000 feet) and ultra-deepwater (>5,000 feet) plays, where massive reservoirs like those in the Miocene, Wilcox, and Norphlet trends hold billions of barrels.

This shift inherently required fewer rigs. Deepwater projects are high-capital-expenditure (high-capex) endeavors, often involving fewer but larger-scale developments like subsea boostin and tiebacks to existing platforms or new floating production systems. For example, a single deepwater well can cost $100-200 million and take months to drill, compared to shallow-water wells at $10-20 million each. As a result, operators have consolidated activity around a smaller fleet of advanced drillships and semisubmersibles that can handle extreme depths and conditions.

By 2025, the average contracted rig count in the GoM was around 22 (mostly drillships), down from much higher numbers in the early 2000s, when shallow water drilling was much more active. Ironically, oil production in the GoM has actually held steady or grown during this time, averaging around 1.8–1.9 million barrels per day in recent years, thanks to these efficiencies.

Technological advances

More capable rigs have meant that fewer are needed. Most modern rigs are vastly superior to those from 10-20 years ago, enabling one rig to accomplish what might have required several in the past. This “efficiency revolution” has been a key driver of the rig count decline, as rigs now drill faster, farther, and in harsher environments, boosting output per rig while reducing the overall fleet size.

Some of the key advances include:

Directional and horizontal drilling. Advances in rotary steerable systems and measurement-while-drilling (MWD) tools allow rigs to drill deviated or horizontal wells extending 5-10 miles laterally from the surface location—far beyond the mostly vertical wells of the early 2000s. This means a single rig can access multiple reservoirs from one wellbore, draining larger reservoirs without relocating. In the GoM, this has enabled “extended-reach” drilling, where one well can replace several older ones, directly contributing to lower rig counts. For instance, recent projects use high-volume hydraulic fracturing and advanced completions to enhance recovery from tight formations, further amplifying productivity.

HP/HT equipment and BOPs. Post-2010 Deepwater Horizon, regulations mandated stronger BOPs (now often rated to 20,000 psi or “20K technology”), along with real-time monitoring and shear rams capable of cutting through thicker casings. This has made rigs safer and more reliable for HP/HT environments like the Norphlet, where temperatures exceed 350°F and pressures hit 15,000-plus psi. Modern drillships are equipped with dual-activity derricks (allowing simultaneous operations), automated pipe handling, and AI-driven optimization, cutting drilling time by 20-40% per well. As a result, the US oil industry now achieves record production with 65% fewer rigs than during the 2014-2016 peak, a trend amplified with the GoM’s deepwater focus.

Overall efficiency gains. Automation, better seismic imaging (e.g., 4D surveys), and data analytics have reduced non-productive time, allowing rigs to complete wells in weeks instead of months. The deepwater GoM recently averaged about 40 oil wells per quarter with just 20 rigs, illustrating how tech has decoupled rig counts from production volumes.

In essence, one modern rig can “do the job(s) of many” from the past, leading to a structural decline in counts.

Other contributing factors

It isn’t just advanced technology driving these trends. While rig capabilities explain a big part of the “fewer but better” dynamic, the decline is multifaceted. Other important dsrivers are listed below.

Economic pressures and oil price volatility. Major crashes in 2014-2016 (oil dropping below $30/barrel) and 2020 (COVID demand slump) forced operators to slash capex, idling rigs. Even with prices recovering to $70-80/barrel, market saturation makes companies hesitant to add supply that could depress prices further.

Flat demand, rising costs. Inflation in steel and labor, and investor demands for returns over growth have kept activity subdued.

Competition from onshore shale. The Permian Basin boom since the mid-2010s diverted billions in capital to quicker, cheaper onshore drilling (e.g., horizontal fracking in shale plays). Shale wells can be drilled in days for $5-10 million, versus months for offshore, making the GOM less attractive for short-cycle investments.

Regulatory and political hurdles. The 2010 Macondo blowout led to a drilling moratorium, dropping rigs from 41 to 19 almost overnight, followed by stricter rules that raised costs and slowed permitting.

Recent policies. In recent years, pauses and cancellations of lease sales have added uncertainty, though offshore is making a modest comeback as shale growth slows.

Basin maturity and decommissioning. With fewer new shallow-water finds, operators are decommissioning old platforms (hundreds since 2000), shifting to infill drilling and tiebacks that require even fewer rigs.

The declining rig count in the US GoM since 2000 has been a “perfect storm” of efficiency gains from tech-savvy rigs, the deepwater pivot, and external pressures. But in many ways, this reflects a more mature, productive industry. Crude oil and gas production in the US GoM could even rise modestly in 2026 with new tech like 20K systems unlocking deeper plays.

The HP/HT effect

Many of the major plays left in the Gulf of Mexico are high temperature and/or high-pressure reservoirs, and these conditions place new requirements on a rig. This, in turn, has been part of the "weeding out" process, leaving fewer active rigs in the Gulf.

The major remaining plays and development opportunities in the US Gulf of Mexico (as of early 2026) are increasingly dominated by high-pressure/high-temperature (HP/HT) reservoirs — particularly those requiring 20K technology (equipment rated for up to 20,000 psi wellhead pressures, often combined with temperatures >350°F). This has indeed contributed to the rig count decline by creating a higher technical bar that only the most modern, capable (and typically newer) rigs can meet, effectively limiting the active fleet to a smaller, elite group of ultra-deepwater drillships and semisubmersibles.

Current major plays

The GoM’s remaining frontier and growth potential is concentrated in deeper, hotter, and higher-pressured zones, as shallower and more conventional plays have largely matured or been depleted. These plays include:

Lower Tertiary/Paleogene Wilcox (Inboard Trend). This is now a flagship HP/HT play, with recent/ongoing developments like Chevron’s Anchor (first 20K production started in 2024), Beacon’s Shenandoah (online in 2025), and upcoming projects like Beacon’s Monument (2026), Shell’s Sparta (2028), and BP’s Kaskida and Tiber-Guadalupe (late 2020s/2030) projects. These target extreme depths (>30,000 ft total) with pressures up to 20,000 psi — a big step up from the previous 15K limit.

Upper Jurassic Norphlet. These plays are high-temperature dominant (often >350–400°F), with some H/PHT elements. Key projects include Shell’s Appomattox (already producing), Chevron’s Ballymore (started 2025, tied back to Blind Faith), and nearby backfill like Dover. Norphlet reservoirs are buried deep and hot, requiring advanced thermal management and HP/HT-rated gear.

Miocene and other deepwater trends. While not always ultra-HP/HT, many remaining Miocene opportunities (e.g., subsea tiebacks) are in ultra-deep water (>5,000–9,000 ft) and benefit from the same advanced tech suite. However, the biggest growth drivers in 2025–2026 (e.g., Whale, Salamanca/Leon-Castile) lean toward these challenging conditions.

These plays are unlocking billions of barrels that were previously inaccessible or uneconomic, driving GoM deepwater production toward record highs – around ~2.2 million boe/d projected for 2026. But these plays demand specialized capabilities that older or less-equipped rigs simply cannot provide.

This shift has acted as natural “rig filter” – weeding out those rigs that are not as new nor as capable, in the following ways:

Rig capability requirements. Drilling and completing in these environments needs 20K-rated BOPs, stronger casings, real-time monitoring, dual-activity derricks, enhanced cooling systems, and automation to handle extreme pressures/temperatures safely and efficiently. Post-2010 regulations (after Macondo) further raised the bar with mandatory HP/HT compliance.

Only modern rigs qualify. The active GoM fleet is now almost exclusively 6th- and 7th-generation drillships/semis (e.g., from owners like Transocean, Noble, Valaris, Stena Drilling). These are often built or upgraded post-2010, with recent retrofits specifically for 20K (e.g., Stena Evolution upgraded for Shell’s Sparta). Older jackups or mid-water semis from the shallow-water era cannot compete here — they are either stacked, scrapped, or repurposed elsewhere.

Fewer rigs needed overall. One of these high-spec rigs can drill/complete complex HP/HT wells faster and more reliably than multiple older rigs could in simpler plays. Combined with the focus on fewer, larger projects (e.g., FPUs with subsea tiebacks), the basin sustains or grows production with just 11–15 rigs (recent counts ~11–13), down from 100+ in the early 2000s.

This “elite fleet” dynamic reinforces the efficiency story: the GoM is more productive than ever, but it runs on a much smaller, more sophisticated rig population. Activity, of course, has not vanished — it has evolved into something far more technically demanding, weeding out anything less than cutting-edge.

This article is part of Offshore's 2026 Gulf of Mexico Regional Report.

About the Author

Bruce Beaubouef

Senior Lead Reporter / Managing Editor

Bruce Beaubouef is Managing Editor for Offshore magazine. In that capacity, he plans and oversees content for the magazine; writes features on technologies and trends for the magazine; writes news updates for the website; creates and moderates topical webinars; and creates videos that focus on offshore oil and gas and renewable energies. Beaubouef has been in the oil and gas trade media for 25 years, starting out as Editor of Hart’s Pipeline Digest in 1998. From there, he went on to serve as Associate Editor for Pipe Line and Gas Industry for Gulf Publishing for four years before rejoining Hart Publications as Editor of PipeLine and Gas Technology in 2003. He joined Offshore magazine as Managing Editor in 2010, at that time owned by PennWell Corp. Beaubouef earned his Ph.D. at the University of Houston in 1997, and his dissertation was published in book form by Texas A&M University Press in September 2007 as The Strategic Petroleum Reserve: U.S. Energy Security and Oil Politics, 1975-2005.