Deepwater opex decreasing in South America, report finds

Offshore staff

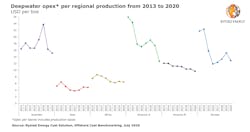

OSLO, Norway – South America has made a cost-cutting leap since 2013, when it was the world’s most expensive region for deepwater oil and gas production costs. Average opex/boe has more than halved since then, from roughly $26 to $12.7 in 2020, according to Rystad Energy. The region also enjoyed the largest cost decline globally this year, in both absolute and percentage terms.

South America’s deepwater opex is driven mainly by Brazil, which accounted for roughly 99% of the continent’s brownfield costs from 2013 to 2020. Petrobras alone accounted for nearly 88% of South America’s deepwater opex, the consultant claimed.

One of the factors that have helped Brazil save opex is Petrobras switching out its FPSO fleet. When the state player initially began production on presalt basins it chose to rent most of its fleet, which led to a surge in its operational costs. In 2015-2016 the company started ordering more owned FPSOs.

According to the consultant, Petrobras increased its fleet of owned FPSOs by 16 while reducing the number of leased FPSOs by six from 2013 to 2020. Eight out of 10 fields in Brazil with start-up years from 2018 to 2020 have been developed via owned FPSOs while the two remaining fields use leased units.

Spurred by the current COVID-19 market volatility and turmoil in the energy industry, Petrobras has also cut its employee count by roughly 22% this year by way of buyout programs. The company plans to achieve total cost cuts of around $2 billion in 2020 by lowering its overhead and relinquishing unnecessary office space.

Another important driver for the reduction in opex in South America is a 55.2% drop in the value of the Brazilian real (BRL) against the US dollar (USD) exchange rate since 2013. This has reduced opex/bbl as the costs are incurred in BRL but paid in USD. Therefore, the depreciation in the real has helped offset local price inflation pressures for general goods and services, the consultant said.

Petrobras has also increased its oil and gas production from 2013 to 2020, which has driven the opex/bbl down further thanks to economies of scale. Looking at this from a global and more generic perspective, already producing fields are generally more likely to have lower opex.

In addition, the portfolio of producing fields in South America has been getting younger, and newer fields require much less maintenance than mature fields that generally have higher operational costs. More than 110 mature fields have been abandoned on the continent over the past eight years, with new fields now accounting for more than half of the total production in South America compared to 17% from very mature fields.

In general, the production share from fields that have passed half of their lifetime has decreased drastically in South America since 2013. According to Rystad, it will be interesting to see the cost profiles of Brazil and Petrobras when decommissioning of older fields starts in a few years, given the country’s lack of experience in this area.

Matthew Fitzsimmons, Rystad Energy’s Vice President Energy Service Research, said: “Looking towards the future, we expect deepwater opex per barrel to stay relatively flat through 2020 to 2021. However, after 2021 we see lifting costs per production increasing by roughly $4 per boe, staying at that level through 2024 with an increase of approximately $1 in 2025.”

The COVID-19 inflicted uncertainty means that service companies, operators and investors will continue to watch their budgets and stay clear of any non-profitable or high-risk projects in the months and years ahead. Due to the generally low and turbulent Brent spot price this year, investments and projects that do not meet the cost and risk criteria set forth by the companies are likely to be delayed, the consultant claimed.

Attaining the lowest possible cost per production will be more vital than ever, despite the fact that cost reductions like the ones seen in 2014-2016 are unlikely as many of the possibilities have already been exhausted. Cost reduction strategies adopted by South America, and more specifically Brazil, could serve as a roadmap for other struggling regions and countries, the consultant claimed.

08/19/2020