NPD foresees steady stream of Norwegian field developments

Offshore staff

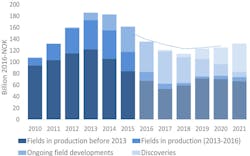

OSLO, Norway – Investments across the Norwegian shelf last year totaled NOK135 billion ($15.85 billion), NOK50 billion ($5.86 billion) less than the peak years 2013 and 2014, according to the Norwegian Petroleum Directorate (NPD).

Spending may remain relatively subdued through 2018, but is then likely to pick up again, NPD believes.

Last year, five plans for development and operation (PDO) were submitted, with a total investment value of NOK23 billion ($2.7 billion). Seven Norwegian development projects are currently in progress with a total value of NOK233 billion ($27.3 billion).

Following several years of high exploration activity, 36 exploration wells were drilled in 2016, 20 down on the preceding year. There were 18 discoveries, one more than in 2015, of which 14 discoveries were in the North Sea, with two each in the Norwegian Sea and theBarents Sea.

NPD’s director general Bente Nyland said: “Many of the discoveries are small, but most are located near existing infrastructure. This means that they can quickly become profitable developments if they are tied in to operational fields and facilities.”

According to Nyland, the pace of exploration activity going forward is uncertain. It depends on how much operators follow up on new discoveries, and the take-up of new exploration acreage.

“It is very important to maintain exploration activity at a high level in order to maintain stable production in the future,” she added.

Last year 56 production licenses were issued under Norway’s APA 2015 round and 10 underthe 23rd licensing round, the latter all in the Barents Sea. The first exploration well in the newly opened southeastern Barents Sea should spud shortly.

The probability of making new big discoveries is also highest in this area, Nyland said: “New surveys also indicate significant opportunities in areas that are not open for petroleum activities.”

Overall spending on the shelf dropped 16% last year, with a further 11% fall anticipated in 2017 to a total of NOK120 billion ($14 billion). A further 5% dip is likely during 2017-18, in part due to lower activity, but also to the general reduction in oilfield service costs.

Future start-ups and new field developments should push investments upwards again from 2019 onwards.

Over the next three years,Gina Krog, Aasta Hansteen, Martin Linge, and Phase 1 of Johan Sverdrup will all come onstream, in addition to smaller-scale subsea developments of the Maria, Utgard, Byrding, Dvalin, Trestakk, and Oda fields.

Other major new development projects are under evaluation such as Johan Sverdrup Phase II,Johan Castberg in the Barents Sea, Snilehorn, Pil, Snefrid North and Skarfjell.

In 2016, Norway’s offshore oil production rose for the third consecutive year and the start-up ofGoliat means the Barents Sea is for the first time contributing to oil output. Gas production is expected to remain relatively stable over the next few years.

This year, overall production should be similar to the total in 2016, around 1.62 MMb/d. A decline is then likely until 2020, when Johan Sverdrup begins ramping up.

However, there is uncertainty in the forecast related to drilling of new wells, start-up of new fields, reservoirs’ ability to deliver, and the regularity of fields in operation.

This year NPD forecasts around 30 exploration wells across the shelf, and the continued downward drift is a concern, the association says, as new profitable resources need to be proven to sustain oil and gas production beyond 2025.

However, the number of applications and awards in the most recent licensing rounds shows interest remains strong in the Norwegian shelf, and several of this year’s planned wells in 2017 are potentially high-impact.

There was little exploration activity in the Norwegian Sea last year, but an upturn is likely this year, including a deepwater wildcat well that may provide additional resources for the Aasta Hansteen development.

More than half of Norway’s undiscovered resources are in the Barents Sea, which is also where the most anticipated wildcats are due to be drilled this year.

Last year one PDO was approved forOseberg Vestflanken 2 in the North Sea, where 110 MMboe will be produced from an unmanned wellhead platform at a cost of NOK 8.2 billion ($960 million), with start-up scheduled for 2018.

This is the first of three planned phases for the remaining reserves in the Oseberg area. Yet to be developed resources from Oseberg, Oseberg South, and Oseberg East are estimated at 850 MMboe.

NPD forecasts that around 10 PDOs will be submitted over the next few years. In 2017 it anticipates PDOs for Johan Castberg in the Barents Sea and the further development of the Snorre field in the North Sea.

Next year, the PDO for Johan Sverdrup Phase II is likely to go forward.

The new development of Snorre, which started production in 1979, involves adding six new subsea templates tied in to the two existing platforms, increasing recovery from the field by nearly 30 MMcm of oil, equivalent to the size of the Goliat field in the Barents Sea. The lifetime of the field should be extended to 2040.

Finally, four North Sea fields were shut down in 2016: Varg, Volve,Jette, and Jotun. ExxonMobil will still use parts of the Jotun field, Jotun A/FPSO for operation of the Ringhorne and Balder fields.

NPD received cessation plans for three more North Sea fields: Oselvar,Gyda, and the old living quarters platform on Valhall. In 2016, the Ministry of Petroleum and Energy also made disposal decisions for the following facilities: Varg, Skirne, Atla, Ekofisk 2/4 C and Tor 2/4 E, Jette, and Jotun.

01/16/2017