Innovation can sustain deepwater market at current prices

Costs must be brought down to align with a 3% inflation rate

Gautam Chaudhury

Consultant

Deepwater projects can be developed at current oil prices if industry stakeholders act together to cut all costs down to realistic levels. It has been done before: the industry has shown great ability to overcome economic challenges in past downturns.

Economic fundamentals alone (supply vs. demand) do not govern commodity prices anymore - those days are gone forever. Prices of commodities are essentially manipulated and controlled by a few big unregulated financial institutions, hedge funds, derivatives, and other speculative forces that play by their own rules of engagement. This is similar to how the stock price index bubble moves up and then gets corrected down. The overall long-term price trend remains a basic inflationary increase within the ups and downs of supply and demand. In between, speculation-driven price trends go up and down at a lower frequency; and the occasional nose dive is a so-called price correction.

The oil and gas industry is no exception to this phenomenon. The trend in oil price consists of three parts: a long-term steady inflationary rise; a short-term (days and months) supply and demand interaction; and occasional external (mostly derivative-driven) speculative force lasting a few years. In the energy sector, there are other minor factors, such as strict emission control and advances in renewable clean energy, affecting the price of oil.

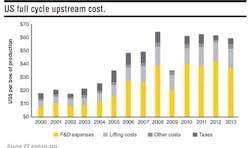

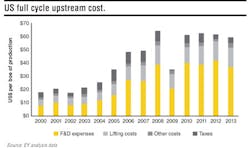

During the last decade, capex and opex have risen steadily at nearly the same pace with the price of oil. Full-cycle costs are up about $60 to $65/bbl from about $18/bbl in the year 2000. This is not sustainable. It is imperative that production costs come down equivalent to realistic oil prices. Visionary leadership must challenge the business as usual and promote a culture of innovation to technology, safety, and operations to reduce cost, increase recovery, and improve safety.

All stakeholders in the oil and gas industry (operators,drilling contractors, consulting engineers, installation contractors, and service contractors) will have to adjust and learn to sustain with reasonable profit at the basic inflationary trend in oil price. This means that the industry must be able to support capex, opex, plus a profit at the baseline oil price. Part of the find and development (F&D) cost may come from the extra revenue generated from the increased price driven by speculative force of the derivative market. This is likely going to be the “new normal” of the industry.

A new innovative subcontract service, proposed below, may offer a strategy for reducing the lift cost part of opex, and can probably help improve the cost and schedule of brownfield work.

Price structure

Oil price volatility is nothing new, but the recent decline and fluctuation at relatively low levels is something the industry may have to deal with for some time. So what is the expected price of oil in 2016 and beyond? A review of expert opinions reveals that there are various schools of thought on predicting oil prices. Projections range from as low as $20/bbl to as high as $200/bbl with respective justifying scenarios. Yes, any price has a probability, however small that may be; but no one has the crystal ball to accurately predict oil prices in a globalized economy that is subject to diverse geo-political constraints, and pressured by speculative forces. The industry must be pragmatic and learn to live according to most probable price, which must be based on the basic inflationary trend over a long period of time, and supply and demand fundamentals.

The most probable long-term price trend will follow economic fundamentals in terms of supply and demand, with an inflationary rise, unless disturbed by other external forces. Supply and demand-related price changes will get corrected reasonably quickly. This is clearly visible in the price trend over the last 30 years, which never fell below the inflationary trend value. There were several significant upward moves due to speculation-driven derivative market pressure.

If we consider a 30-year period and start with an average price of $18/bbl in 1986 and apply a 2%, 3%, and 4% inflationary increase, the expected prices in the year 2016 are $32.6, $43.7, and $58.4/bbl, respectively. This means, an average price of $44/bbl, based on 3% inflation, may be considered as the “new normal” price. A 3% inflation rate is a good long-term representative value. In the last 100 years, the average stock market price index has moved at a 3% average inflation equal to 19.21 times (1.03^100) from about $900 to about $17,300.

Even though the current price ($44/bbl at press time) is low, it must be realized that this is a sustained average lower bound price. It is unlikely that an average price in any year will decrease further as the pressure of economic fundamentals (supply and demand) will ensure that. If anything, yearly average prices are likely to be higher for various reasons as described above. Thus, there is a good confidence in the $44/bbl minimum average price.

Production costs

Between the 2004 and 2013 total upstream spending has increased steadily at about 13% per year, and the operating/production or lift cost has also increased at about 10% per year, except for the global financial collapse in 2008/2009. These rates are unreasonably high. Even the 2008/2009 figure is higher compared to the yearly 3% inflationary increase. This was possible because of continued rise in oil prices.

It is interesting to note that, around the year 1996/1997, Shell’s Auger and other contemporary fields in around 1,000-m (3,280-ft) water depths in theGulf of Mexico (GoM) were profitable at about $20/bbl. When BP’s Atlantis and Chevron’s Blind Faith were sanctioned in 2005, the price was about $25/bbl. In fact, oil companies were making more profit at lower oil prices in the near past than recently at higher oil prices. Based on this data, the industry should be able to make do with a price of $44/bbl, although the general consensus is that at least $65/bbl is required. Most likely, a higher price is required depending on the size of fields; the difficulty associated with reservoirs; and the operating company overhead structure. But what has changed?

The answer to that is: water depth has doubled; subsea tieback distances have increased; and some reservoirs may be difficult, uncertain, or have higher temperature and pressure. This may result in more money spent on research and development. Still, these factors alone do not justify the escalation of capex and opex to the high level that the industry now faces. For example, the cost of Shell’s Auger was $1.2 billion (1997) in 1,000-m water depth; the cost of BP’s Atlantis and Chevron’s Blind Faith in 2,200-m (7,217-ft) water depth were about $1.8 billion (2005); whereas the cost ofChevron’s Jack/St. Malo project, also in 2,200-m water depths, was $8 billion (2015).

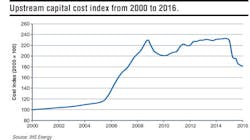

It is clearly visible that capex inflation followed the same exponential increase as oil prices were buoyed by speculative pressures. In addition, opex has also followed the same trend. This is not sustainable. Costs should not have gone up at the same rate as the speculative price of oil. Total breakeven costs went up by 17.4% per year from 2000 ($18/bbl) to 2008 ($65/bbl). This has resulted in a continued decrease in sanctioned projects. Now costs must come down. That is to say, whatever corrections are needed must be made for the survival and sustainability of the industry. The downward trend on cost has started, but it still has a long way to go to be realistic. We need to challenge all elements of capex and opex and bring them down equivalent to the year 2000 by innovative means.

Survive and sustain

Companies in some countries can still make substantial profit at a price of $44/bbl because of their uniquely easy and low risk reservoirs and respective associated low capex and opex. There are other countries where it appears that companies may not be profitable at this price. The US GoM is one such location. If one reviews the breakeven cost per barrel in the US market, one can see that there has been little change in this metric since 2010.

Generally, oil economics are presented in terms of cost per barrel; thus, it is highly dependent on total net recovery barrel and the field life. Let us examine the economics based on a medium-size field of 250 MMbbl of net recovery in 20 years, which is equivalent to about 40,000 b/d, assuming a few days of lost production per year. From the $44/bbl price, we can safely allocate $40/bbl to cover all costs, leaving a good 9% profit margin [(sales - cost)/sales]. The average profit for other industries is around 7%. The cost of capital can be taken as 2.5 times the initial capex investment, based on 20 years of uniform repayment at 10% interest.

If capex follows the same 3% increase, then a $1.8-billion cost in 2005 should now (2016) cost $2.5 billion. Based on a 10% discount rate, total capex spread over in 20 years is nearly 2.5 times, say $6.25 billion. That is $25/bbl, based on a net recovery of 250 MMbbl. The revenue of $25/bbl is equivalent to net NPV of zero for the capex. This leaves $15/bbl, which should leave a good margin after opex. If we follow the same 3% inflation, total full-cycle cost in 2016 comes to $29/bbl (18*1.03^16), starting from $18/bbl in 2000. Both methods give comparable results. This confirms that costs must be brought down. There is still a hidden benefit left. The $44/bbl oil price considered is for 2016, but the average price over 20 years, based on 3% inflation, is $62/bbl. Only the opex will be offset at 3% per year cost increase, assuming all things remain the same.

There is a high probability that occasionally prices are likely to increase beyond the average inflationary fundamentals due to speculative market pressure and other disruptive forces; or, if and when supply is threatened as a result of industry capex investment falling behind due to lack of resources. In the long term, one way or the other, a shortfall in capex will come from higher oil prices, directly or indirectly.

Most of the above cost increase is from drilling and completion, platforms, subsea and process equipment, installation contractors, and layers of overhead in all areas. Operating companies are no exception. The last decade of unrealistic high oil prices has resulted in profligacy and complacency in all areas of the oil and gas value chain. A natural correction is inevitable everywhere, including the other service sectors. Recent actions by the oil majors are showing good reduction in opex. Much more is needed considering that recent past completed projects are carrying high capex liability as their spend amounts were based on higher oil prices. Therefore, innovation all around is the key to survival and sustainability, even at $44/bbl base price (as of 2016), provided that costs are brought down in line with prevailing inflation.

New service contract

The innovative ideas to bring operating costs down should not only be limited to mergers and acquisitions, consolidations, or technology areas in terms of drilling, production, facilities, and processing. It must also extend to include routine sustainable engineering (structural and naval architectural) and operational management of real estate assets (fixed or floating), thereby reducing opex overhead. Simply put, sub-contracting to small companies with efficiency and low overhead should be done whenever possible. This is similar to service contracts for assets integrity management. Savings of at least 50% can be easily achieved, and could even be more depending on the type of contract, extent of service, and number of clients served by a sub-contractor.

Routine non-sensitive activities of floating asset operations and maintenance for drilling and installation contractors and operating companies should be identified. Examples include site and job-specific vessel capability assessment, routine stability checks and structural checks with respect to changes in operation, and other small modifications when required. The sub-contractor must have engineers highly experienced in multidisciplinary areas with strong in depth knowledge and confidence, as the pressure of work turnaround necessitates its speedy completion. It must be appreciated that, in operational situations, sometimes there is very little time to wait, unlike in cases of design activities. A different breed of engineers with deep understanding, challenging spirit, and lateral thinking are needed, at least, as a mentor and quality assurance guide.

Typically, a service contract is made to perform routine sustaining engineering and other agreed-to activities. Generally, it is simple and better with a lump-sum per year contract, depending on the number and type of assets and anticipated volume of work.

However, other forms of contract may work as well. Actual logistics of work flow management, quality assurance, traceability of work, and documentation control have to be agreed, established, and aligned with respective systems of operations in place. Once a contract is placed, the sub-contractor allocates dedicated engineers for immediate attention to client’s work need. At least once, this type of contract was successfully applied in the mid 1980s between a drilling company and a consulting engineering company.

These types of service contracts may be extended to other types of activities as well, should opportunities exist. The possibility can be evaluated by respective companies based on the nature of their operational activities. The cost benefit comes from consolidation of work and reduced layers of overhead of small service companies, as opposed to the high overhead cost of major operating or contracting companies.

In some ways, the system works like an insurance concept, especially when there are multiple contracts with different companies. Once such a system is in place, it may also be extended to brownfield activities, which could thereby benefit from reduced administration costs and shorter schedules.

The confidentiality aspect, in terms of platform and vessel details, should not be a concern at all. Consulting engineers, contractors, and sub-contractors simultaneously work on multiple projects from different clients without divulging information, a professional code of conduct. Besides, in most cases, there will be no sensitive information on the type of work depicted here.

Conclusions

US deepwater projects can be economically viable at current oil prices, provided costs can be brought down to a level aligned with the realistic 3% inflation. It will require dedicated leadership, good discipline and control on capex and opex, and innovation in technology and operations from all stakeholders through the full cycle of the oil and gas industry. It is a paramount challenge.

Now is the time to reorganize and restructure to become lean and efficient, verify, validate, and to implement cost saving operational procedures such as innovative sub-contracting.

Empowered champions with vision must take the lead to step changes in technology and in operations, challenging the status quo. Otherwise, the high cost of deepwater development will continue to be a barrier to future projects, especially in the cases of smaller fields.

The industry cannot wait for oil prices to rise so that they can match the present level of cost. Rather, we need to proactively learn to live with the “new normal” price. From time to time, the price will rise to more than $44/bbl due to outside influences, and that will be windfall gain. Such gains should then be used wisely. Perhaps, spending a portion in future research will improve safety, reduce cost, and increase net oil recovery.