Analyst revises long-term oil demand forecast

Offshore staff

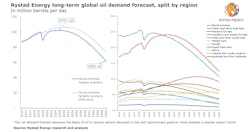

OSLO, Norway – The COVID-19 pandemic and the acceleration of the energy transition have led Rystad Energy to revise its long-term oil demand forecast. The virus is expected to have a lasting impact on global oil demand, which it now sees peaking at 102 MMb/d in 2028. Before COVID-19, the consultant had called for peak oil demand of just over 106 MMb/d in 2030.

Rystad examines three different scenarios in its long-term oil demand prognosis, and peak demand at 102 MMb/d in 2028 is the most likely outcome. This forecast scenario is called the “Governmental Targets Scenario” and assumes the share of oil in various sectors develops in line with stated government goals to move toward a cleaner carbon future, notably in the electrification of transport.

Meanwhile, the persistence of the COVID-19 pandemic is likely to cause 2020 oil demand to decline to 89.3 MMb/d, compared to 99.6 MMb/d in 2019. Demand will then recover to 94.8 MMb/d in 2021 still capped by regional lockdowns and slow international aviation recovery as airlines continue to operate far below pre-virus levels.

In its Governmental Targets Scenario, oil demand then recovers to 98.4 MMb/d in 2022, still stuck below pre-virus levels due to structural COVID-19 impacts such as less work commuting and slower aviation recovery. It is only in 2023 that demand will recover to pre-COVID-19 levels and jump back to 100.1 MMb/d.

Artyom Tchen, Senior Oil Markets Analyst at Rystad Energy, said: “The slow recovery will permanently affect global oil demand levels, shaving at least 2.5 MMb/d off our forecasts made before the coronavirus. We have lost at least two years of oil demand growth in 2020 and 2021, while before the virus we expected yearly growth of 1 MMb/d. The lockdowns will stunt economic recovery in the short term and in the long term and the pandemic will also leave behind a legacy of behavioral changes that will also affect oil use.”

Supplementing the effect of COVID-19 on oil demand, the consultant said the energy transition is accelerating and weighs on its peak oil demand revision. All sectors contribute to the transition, but transport (60% of oil demand) will be the ultimate driver of this shift. By 2025, the plug-in-hybrid and battery electric vehicles (EVs) are expected to achieve 14% market share in new passenger vehicle sales, according to public governmental targets, then further grow to 80% by 2050.

In the short and medium term, the consultant also accounts for an indirect impact of COVID-19 on oil demand prompted by individual behavioral changes. Although some more months will be needed to fully assess how the pandemic has reshaped peoples’ habits and companies’ business models, it already observes some behavioral headwinds to oil demand recovery from slower rush-hour traffic recovery in summer, an indication that a fraction of commuters will continue working from home even after lockdowns are lifted.

The consultant expects this behavioral headwind to visibly cap demand recovery toward 2023. On the aviation side, the behavioral barriers to oil recovery can be even stronger as cost-cutting policies and teleconferencing may cap aviation business travel recovery, while it also expects some leisure travelers to abstain from airborne travel in the first years following the pandemic.

The consultant sees a sustained commitment from vehicle manufacturers and governments to meet electrification and CO2 abatement targets, little changed even by the economic turmoil brought by COVID-19. This proves the resilience of the ongoing technological developments; however, oil substitution effects are yet strong enough to derail oil demand from recovering to pre-virus levels and then growing for a few years to come.

Between 2025 and 2030, oil demand will enter a plateau phase at around 102 MMb/d, the consultant claimed. In this phase, it no longer sees any residual COVID-19 impacts. It expects firm structural demand growth driven mostly by developing Asia and Africa, which will push demand up, and an increasing, yet weak substitution impact in the road transportation segment as well as a continued structural decline in the power, industry and buildings sectors, which will drive demand down. In this phase, it estimates that these effects will roughly net each other out.

The post-peak phase (2030-2050) is characterized by the acceleration in EV adoption and recycled plastics use, which will also spill over to developing countries and satisfy part of their energy demand. In the very long-term, the consultant sees a steep decline of oil demand to 62 MMb/d in 2050, driven by the high penetration rate of EVs in the automotive industry. In addition, the convergence of plastics recycling rates to around 70-75% – rates currently observed in other materials such as glass, aluminum cans and iron – will also contribute to that declining trend, albeit at a lesser extent.

The sectors that contribute most to the demand shift from a plateau to post-peak decline are passenger vehicles and trucks/buses. Historically, these two sectors represent the biggest share of oil demand, accounting together for 48% of the total. At the same time, it expects more sustained and prolonged demand support from the aviation segment, where feasible/viable substitution technologies are limited as well as in the petrochemical sector, where only a portion of plastics consumption can be recycled and substituted by bioplastics. In the post-peak phase, the rise of EV adoption will accelerate and spill over to developing countries, contributing to the precipitous demand fall.

Geographically, the demand growth that we observe until 2030 will be driven by Asia, led by China and India. In fact, for many Asian, Latin American and African countries to satisfy economic expansion and middle-class growth plans, oil demand will most probably increase through 2030 in those countries. Afterward, the consultant expects that the energy demand in developing countries will keep increasing, driven by GDP and population growth, but that it will be increasingly satisfied by alternative sources and new technologies in a decarbonization push.

Developing countries in Asia and Africa will see a sustained increase in oil demand through the end of the 2040s in its updated forecast as infrastructure hurdles and heavy discounts on imported used internal combustion engines will make it harder for new technologies to penetrate these regions, particularly in rural areas.

“Overall, we do not believe COVID-19 has put peak oil demand behind us, but we do acknowledge the pandemic will greatly alter the peak oil demand reckoning moment, both in terms of timing and volumes. This will help oil substitution gain speed and inevitably take global consumption to lower levels quicker, hand in hand with the energy transition,” Tchen concluded.

11/02/2020