Top 10 offshore drillers: ADES’ acquisition strategy lands it at top

Key highlights:

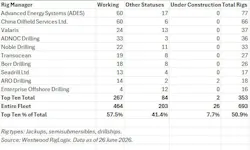

- ADES has become the leading offshore rig manager with 77 units, driven by acquisitions like Shelf Drilling and other pending deals.

- Major mergers, including Transocean's planned acquisition of Valaris, are reshaping the market, with combined fleets expected to reach 64 units post-merger.

- The global rig count decreased from 717 to 693 between 2024 and 2026, with the top 10 managers controlling over half of the fleet, indicating industry consolidation.

- Regional market analysis shows strong dominance in the US Gulf, with 94.4% control by top managers, while Latin America and Asia Pacific remain less consolidated, relying more on local contractors.

By Cinnamon Edralin, Westwood Global Energy Group

Saudi Arabia-based Advanced Energy Systems (ADES), which was the third-largest offshore driller in terms of managed units (jackups, semisubmersibles, drillships) based on figures at the end of 2024, has catapulted itself into the top spot with 77 units currently under its management – and more pending final contract signings.

The former largest manager was China Oilfield Services Ltd. (COSL), which managed 65 units at the end of 2024 and now holds 66 units as of mid-2026.

While ADES is focused on building its offshore drilling rig fleet, this is not the case for most of the drillers on the Top 10 list. The global rig count dropped from 717 at the end of 2024 to 693 as of mid-2026, with the 10 largest managers now controlling 353 rigs, down from 363. However, the effect of recent mergers and acquisitions, along with fewer rigs still in the market, has left the Top 10 controlling 50.9% of the global fleet, a slight increase from 50.6% over the period under review.

Transocean-Valaris merger

Valaris, which was in second place at the end of 2024 with 47 managed units, has streamlined its fleet to 37 units, dropping it into third place. Furthermore, in February 2026, sixth-spot Transocean announced an agreement to acquire Valaris in an all-stock arrangement valued at $5.8 billion. Because this transaction has not yet closed (closing is targeted for the second half 2026), this article continues to treat them as separate companies. Transocean did not change positions on the list since the previous update; however, it too reduced its managed rig count, dropping from 36 to 27.

Assuming no further adjustments to either company’s fleets ahead of closing, the combined company, which will continue under the Transocean name, will have a managed fleet of 64. This figure differs from the 73 units mentioned in Transocean’s acquisition announcement because some units owned by Valaris are managed by ARO Drilling, and one semisub managed by Valaris was sold for recycling after the acquisition was announced.

Other market moves

Borr Drilling has also been busy buying rigs. The company announced the acquisition of five jackups from Noble Corp. in December 2025 for $360 million. The transaction closed in January 2026 and bumped Borr’s owned jackup fleet to 29. Two of these rigs – Forseti (ex-Noble Mick O’Brien) and Bestla (ex-Noble Resolute) are under bareboat charter to Noble until December 2026. Additionally, one of Borr’s rigs is being managed by Etesco Drilling while working off Brazil. These arrangements leave Borr with 26 units currently under its management.

Besides the Noble jackups, Borr is also acquiring all five jackups from Fontis Energy, which is a subsidiary of Paratus Energy, for $287 million. The acquisition will be completed through BC Ventures Ltd., a newly established joint venture between subsidiaries of Borr and its long-term well construction partner in Mexico, CME. All five jackups are currently located off Mexico. This transaction is expected to close in Q3 2026, subject to customary closing conditions, including merger control approvals.

Undelivered rig count

The number of rigs under construction, which includes several long-stranded units, remains at 26. However, there have been a couple of changes since the previous update. In November 2025, ARO Drilling ordered jackup Kingdom 4, for which construction commenced in Q2 2026. Meanwhile, the only delivery since the end of 2024 was the ultra-deepwater drillship Tidal Action, which is owned by Hanwha Drilling and currently being managed by Constellation Oil Services.

The breakdown of the 26 undelivered units is 13 jackups, seven semisubs, and six drillships. Of the 26 rigs, 21 were ordered over a decade ago. Therefore, much of the technology and software is now out-of-date or no longer preferred, which would increase the time and cost to prepare the units for final delivery. It is highly likely that several of these undelivered units will never see the light of day as drilling rigs. Some may be converted for other uses, and some may be cannibalized for steel and other parts.

The rise of ADES

ADES has acquired, or agreed to acquire, 38 jackups since the end of 2024. This was mainly achieved through its acquisition of Shelf Drilling, which was announced in August 2025 and finalized in November 2025. Shelf added 33 units to ADES’s portfolio and increased its international presence. At the end of 2024, only six of ADES’s jackups were outside the Middle East. As of mid-2026, ADES now has 33 units in regions beyond the Middle East, making it truly an international contractor.

Furthermore, in June 2026, ADES agreed to acquire Saudi Arabian Saipem Ltd. from Saipem International for $285 million in cash. This acquisition is expected to close in Q3 2026, subject to regulatory approvals and customary closing conditions. Three of the rigs are owned and two are leased. All but one of the five are currently located in the Middle East. The fifth unit is working off Mexico. Upon closing, Perro Negro 10 will be bareboat-chartered to Saipem so the company can continue managing operations off Mexico and fulfill its contract commitment. As with the pending Transocean/Valaris merger, these five rigs are not yet counted in ADES’s fleet for this report.

Regional market analysis

In terms of regional coverage, the Top 10 managers remain the most dominant in the US Gulf, controlling 94.4%, up slightly from 93.6% in the last report. Transocean leads the way, with eight rigs, all drillships, in the region. West Africa also gained ground from the previous Top 10 update, increasing to 68.0% from 65.0%. West Africa is experiencing a resurgence in demand, and rigs are being moved into the region as a result.

Of the world’s major offshore rig regions, the one where the Top 10 is the weakest is Latin America, where the most active countries of Brazil and Mexico lean much more heavily on local rig contractors for their needs. Asia Pacific is the second lowest at 39.4%, citing the same preference for local contractors from several countries in the region.

Back to ADES

Unless the market sees a mega-merger of multiple companies, then ADES is likely to remain the world’s largest offshore rig contractor in terms of managed fleet size for at least the next few years. As the industry trends towards a leaner, more efficient supply, we continue to expect more consolidation, whether piecemeal by single- or multiple-rig packages, or whole companies.

About the Author

Cinnamon Edralin

Cinnamon Edralin is Americas Research Director for RigLogix, a division of Westwood Global Energy Group, and has been covering the offshore rig market since 2006. She began her career with ODS-Petrodata, which was acquired by IHS (later becoming IHS Markit), where she managed the Americas offshore rig team, along with the Americas marine team and the US/Canada land rig team. Edralin then moved to Esgian, where she helped raise brand awareness for offshore rig services and supported the offshore wind market team. She joined Westwood in 2023 and provides support for the subsea team in addition to her rig analyst duties. Edralin holds a BA in Liberal Arts from the University of St. Thomas in Houston, Texas.