More newbuild rigs find homes in an increasingly optimistic market

Editor's note: This story first appeared in the September-October 2022 issue of Offshore magazine. Click here to view the full issue.

Hans Jacob Bassoe * Esgian Rig Services

The past few years have been tough on the offshore drilling industry and the downturn has adversely affected rig construction, with only five newbuild orders made in the past five years. If that was not bad enough, the arrival of the COVID-19 pandemic caused a series of delays due to stringent travelling restrictions and disrupted supply chains. Also, it led to several newbuild cancellations and forced shipyards to take ownership over the stranded assets. However, we have now passed the trough and there is an increasing optimism in the industry. Finally, newbuilds are finding new homes.

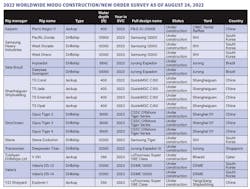

There are currently 54 rigs under construction, most of which are jackups. There are 33 jackups, 6 semisubs and 15 drillships. Out of the 54 newbuilds, 18 rigs are owned or managed by an offshore drilling contractor, while the remaining 36 are stranded assets owned by yards. Only eight newbuilds have been contracted for future work, but we anticipate this number to increase in the coming months as several other newbuilds are rumored to be offered into tenders.

China still holds the lion’s share of newbuilds, ahead of Singapore and South Korea. There are currently 23 rigs under construction at Chinese yards, of which 18 are jackups. Most of the construction contracts have been cancelled and the rigs are now owned by the shipyards. Singaporean yards currently have 14 rigs under construction, 10 of which are jackups. However, five of the rigs are expected to be delivered during 2022 (more on this below). Lastly, South Korea currently has eight rigs under construction, all of which are drillships. Samsung Heavy Industries and Daewoo are constructing four drillships each. All the drillships have delivery dates in 2023, but most will likely be pushed as seven are stranded assets.

While the number of stranded assets has been increasing, the number of newbuild orders has collapsed. Since 2016 there have only been five new orders, two jackups and three semisubs. The semis were ordered in 2018 and 2019, two of which were ordered from KeppelFels by the Norwegian drilling contractor Awilco but who later cancelled both newbuilds. During the pandemic the Saudi Aramco/Valaris joint-venture – ARO Drilling – ordered two jackups to be built by Lamprell and International Maritime Industries (IMI) as part of a larger newbuilding program. The two rigs are the first of 20 jackups ARO Drilling committed to purchase by 2030, which will be locally built by IMI in its Ras Al-Khair yard. We do not expect any new orders to happen in the near-term (besides the commitment from ARO), at least not until most of the stranded assets have been absorbed.

Many of the newbuilds are uncontracted, as most were originally speculative orders or were later cancelled by drilling contractors. However, just this year, seven newbuild jackups have been awarded drilling contracts with Saudi Aramco and two with ADNOC for work in the Middle East. Three of these jackups are being built in China and four in Singapore. Currently, only one newbuild floater under construction, the drillship Deepwater Titan, is contracted. The Transocean drillship is expected to be delivered later this year with a 20,000 psi BOP installed and will commence its five-year contract with Chevron in the US Gulf of Mexico in 3Q 2023. The sister vessel, Deepwater Atlas, was recently delivered and will commence its contract with Beacon Energy in 1Q 2023 and later have a 20,000 psi BOP installed.

The increased activity in the jackup transaction market has not been limited to second-hand rigs, but as mentioned above, newbuild jackups have also changed hands. Except for one transaction, the buyers have been Middle Eastern companies looking for jackups to cover the regional demand. At the beginning of the year, ADNOC Drilling acquired the Mehzem (Ex-Bestford 3) and Bateel (Ex-Bestford 4) from CMHI in China. Both rigs were mobilized to the UAE on three-year contracts (plus options) with ADNOC.

Additionally, both ADES and Arabian Drilling Company have bareboat chartered two KeppelFels owned jackups each, Admarine 683 (Ex-Fecon 1), Admarine 684 (Ex-Fecon 2), Arabdrill 120 (Ex-Fecon 3) and the Clearwater B-Class 4, all of which are contracted to Saudi Aramco with commencement dates in 4Q 2022 (and expected delivery late 3Q). Lastly, Saipem bareboat chartered the CIMC built Perro Negro 11 (Ex-Gulf Driller VII). The jackup, which is also contracted to Saudi Aramco, will be delivered in 3Q 2022 and is scheduled to commence its five-year contract in December 2022.

Furthermore, newbuild floaters are increasingly being acquired by drilling contractors. Last year, Dolphin Drilling secured the rights to purchase the harsh-environment semisubs Nordic Spring and Nordic Winter. The two semis, which were terminated by Awilco during the pandemic, are expected to be delivered in spring 2024 and 2025, respectively. Regarding the drillship segment, Saipem and Samsung Heavy Industries reached an agreement in June 2021 to bareboat charter the Santorini (Ex-Ocean Rig Santorini) including a purchase option. The drillship then later mobilized to the US Gulf of Mexico where it began work for Eni. An additional two drillships have been acquired. A second Samsung drillship, Stena Evolution (Ex-Ocean Rig Crete), was sold for $245 million late last year to Stena Drilling. However, the sale has not yet been finalized, as Stena has until October 2022 to confirm the purchase. Lastly, the DSME-built Abdulhamid Han (Ex-West Cobalt) was acquired by Turkish state operator TPAO in November 2021 for $180 million and later commenced drilling operations in Turkey 3Q 2022.

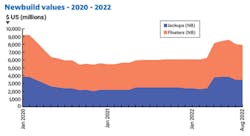

The increasing demand for rigs has had a positive effect on rig values, and newbuild values have risen on an average by over 30% in the last 12 months. Jackup values have increased even more, by almost 50% year-to-date (ytd). Currently, the most valuable newbuild jackups are the ex-Seadrill West Tethys and its six sister jackups, which are being built by DSIC in China. Each jackup is valued by Esgian Rig Values in the range of $114 to $126 million. The value upside on floaters has been more mixed. Newbuild drillship values have increased significantly this year, by over 23% (ytd), while semisubs have had a more moderate increase of 6.4% (ytd). The most valuable newbuild floater, according to Esgian Rig Values, is Transocean’s Deepwater Titan, valued at $341 to $377 million.

Although the offshore industry and the newbuild segment is gaining upward momentum, the four Sete Brasil floater newbuilding projects remain a mystery. The four rigs under construction in Brazil include the two semisubmersibles Urca and Frade, which are built by KeppelFels, and the two drillships Arpoador and Guarapari, which are built by Jurong. In 2019, the Norwegian investor Magni Partners offered to acquire all four floaters, with the local drilling contractor Etesco agreeing to manage the rigs. After the acquisition, the rigs were to be chartered to Petrobras on a 10-year deal with a dayrate of $299,000. However, the transaction is yet to be completed.

Meanwhile, the focus on renewables and the energy transition has made shipyards refocus on renewables and, in particular, the offshore wind industry. Earlier this year, Sembcorp Marine and Keppel Offshore & Marine (a subsidiary of Keppel Corp.) announced their merger agreement, and the new combined entity will focus on offering offshore renewables, new energy and cleaner solutions in the offshore and marine sector. The proposed merger, which is subject to shareholder approval due in 4Q 2022, includes the sale of Keppel’s legacy rigs into an asset company that will be owned 90% by investors, with Keppel holding 10%. In China, SinoOcean has rejuvenated Chinese-built jackups for work in offshore wind. Last year, a JU2000E and a GustoMSC CJ46-X100-D were converted and contracted to PowerChina Guizhou Engineering for offshore wind installation work. Another jackup, built by CIMC Raffles, was also converted to work locally in China.

After a prolonged downturned that was exacerbated by the COVID-19 pandemic, it seems like the winds are shifting. Although the industry is still in recovery, stronger market fundamentals have caused rig utilization and dayrates to increase. As a result, the once abandoned newbuilds are now becoming hot takeover objectives.