Report foresees future of energy super basins linked to renewables

Offshore staff

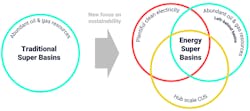

LONDON — A report by Wood Mackenzie finds that energy "super basins" of the future must deliver on three key criteria: abundant resources, access to low-cost renewable energies and hub-scale carbon capture and storage (CCS) opportunities.

As global demand grows for sustainable energy, the upstream industry of the 2030s and beyond will have to focus on where its synergies with new energies are strongest, the consultant claims.

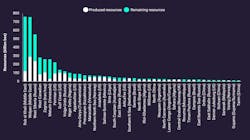

Fewer than 50 traditional super basins—those originally holding more than 10 Bboe, and with more than 5 Bboe remaining—supply more than 90% of the world’s oil and gas.

Wood Mackenzie Vice President Andrew Latham said, “Of the remaining resources from traditional super basins, only 1,453 Bboe or half have been identified as future-fit energy super basins…

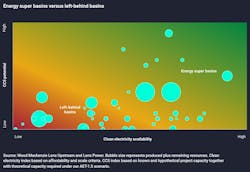

“The upstream industry of the 2030s will have a different footprint as investment migrates to the new energy super basins. With some basins set to be left behind, the industry will become even more concentrated in its top basins. At the same time, upstream strategies will increasingly merge with low-carbon businesses.”

Scope 1, 2 and 3 emissions

Much of the world’s production is operated by companies with net-zero targets for Scope 1 and 2 emissions by 2050 or earlier. Electrifying operations using a clean, renewable energy source is considered one of the quickest and best ways to eliminate emissions.

But the renewable energy sources also need to be plentiful and affordable.

“The co-location of low-cost renewables with low-cost oil and gas is key,” Latham said. “Surplus renewables can also be fed into the grid as part of the overall energy system.”

Scope 3 emissions accounted for more than 90% of oil and gas’ emissions of 18.5 billion metric t/year CO2e in 2021, representing over half of the world’s entire energy-related emissions.

They can be reduced by cutting production or indirectly via sequestration or offsets, with CCS seen as the most promising sequestration technology, since it offers the scale to decarbonize difficult-to-abate consumer sectors and could also save 18% (with direct air capture) of annual global emissions by 2050.

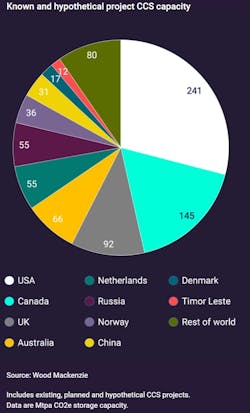

CCS forecast

Although CCS does not need to be in the same basin as oil and gas production, in practice it will be close to upstream operations.

Latham said, “Our assumption here is that this growth will come mainly from countries that will have hub-scale emissions sources available close to subsurface storage options. CCS operators will offer sequestration as a service to emitters.”

Examples of future energy super basins are said to include the US Gulf Coast, the North Sea and Australia’s North Carnarvon Basin.

Wood Mackenzie expects a substantial CCS industry to emerge around the Texas coast, based on hub-scale CO2 sources from refining, petrochemical and other industrial facilities.

Host governments may have opportunities to improve the outlook of a basin, Latham suggested, through carbon taxes and other fiscal and regulatory moves to accelerate decarbonization, especially those that enable CCS.

07.21.2022