Expanding the Gulf of America: A strategic move for long-term energy security

Key Highlights

- The Gulf of America produces about two million barrels of oil daily and supports hundreds of thousands of jobs nationwide.

- Expanding into the South-Central Gulf could add over 470,000 barrels of oil equivalent per day by 2040, supporting economic growth and energy security.

- Development in this region benefits from existing infrastructure, reducing costs and increasing efficiency for operators.

- Maintaining a steady pipeline of new projects is crucial for long-term Gulf output, which requires access to prospective acreage and stable policies.

- The Gulf’s mature basin status underscores the importance of new resource areas to sustain production and competitiveness amid global energy market pressures.

By Erik Milito, President, National Ocean Industries Association (NOIA)

The Gulf of America remains one of the most productive and prospective offshore energy regions in the world. It delivers roughly two million barrels of oil per day, supports hundreds of thousands of jobs across the country, and is backed by a deep network of infrastructure, vessels, ports, and skilled workers that have been built over decades.

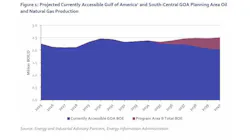

A new report from the National Ocean Industries Association (NOIA) and the American Petroleum Institute (API), prepared by Energy and Industrial Advisory Partners, looks at the impact of expanding development into the South-Central Gulf of America, an area near existing infrastructure in the Central Gulf and distant from the region’s coastline. The findings are clear: opening this area could support more than 133,000 jobs, generate over $11 billion in GDP, and add more than 470,000 barrels of oil equivalent per day in production by 2040. Those gains are incremental to what the Gulf already produces today.

The Gulf of America continues to perform at a high level, but much of today’s production reflects investment decisions made years ago. That is the nature of offshore development. Projects take time to evaluate, permit, finance, and build. From lease to first production can take a decade or more, and once online, assets are expected to produce for decades. The system only works when there is a steady pipeline of new opportunities feeding into it – like a conveyor belt.

Right now, that pipeline is tightening. Recent project announcements have focused on existing infrastructure, with more tiebacks and fewer large standalone developments. Exploration success has become more selective. The Gulf of America will remain important for a long time, but a basic reality remains true: even the most prolific basins need new areas to sustain long-term output.

That is where the South-Central Gulf of America comes in.

From an operational standpoint, it is not a new frontier in the traditional sense. It sits adjacent to existing infrastructure and can leverage the same workforce, supply chain, and technical capabilities that support current Gulf operations. That matters. Development in areas with established systems is more efficient, more predictable, and generally lower cost than starting from scratch elsewhere. It also allows companies to build on what they already know about the basin.

From an investment standpoint, access to new acreage is equally important. Offshore projects require large, long-term capital commitments, along with a large portfolio of leased acreage. Companies and their investors are making decisions based on multi-decade timelines. They look for regions where the resource potential is strong, infrastructure is in place, and policy frameworks are stable enough to support development over time. The Gulf of America meets those criteria today, but maintaining that position requires continuity.

Opening the South-Central Gulf sends a clear signal that the United States intends to keep the Gulf competitive as a destination for that kind of investment. Without that signal, capital may not disappear, but it can shift. Other offshore provinces, both in the Western Hemisphere and beyond, are competing for the same dollars.

There is also a broader supply picture to consider. Energy demand continues to grow, driven by industrial activity, population growth, and emerging technologies. Conflicts in the Middle East and Eastern Europe have rocked oil markets. At the same time, supply chains are under pressure from geopolitical instability. In that environment, the ability to produce energy domestically, under established regulatory and environmental standards, carries strategic value.

The Gulf is well positioned on that front. US offshore production benefits from strong safety and environmental oversight, and its production has the lowest carbon intensity in the world. Expanding development in the South-Central Gulf builds on those advantages.

None of this changes the fact that the Gulf of America is a mature basin. That maturity is a strength, as it reflects decades of successful development, but it also means that maintaining output requires a consistent flow of new projects. Access to additional resource areas is part of that equation, along with predictable leasing and permitting processes that allow companies to plan ahead.

The alternative is not an immediate drop-off in production. It is a gradual tightening of the project pipeline, potentially fewer large developments over time, and a reduced ability to grow output when market conditions call for it. Those trends play out over years, not months, which is why they are often overlooked until they become harder to reverse.

The opportunity in the South-Central Gulf is to stay ahead of that curve.

The Gulf of America has been a cornerstone of US offshore energy for generations because it has combined resource potential with infrastructure, expertise, and a regulatory system that—when functioning predictably—supports long-term investment. Extending access to adjacent areas is a continuation of that model, not a departure from it.

For companies operating in the Gulf of America, the path forward is straightforward. It depends on having access to prospective acreage, the ability to evaluate and develop it over time, and confidence that the policy environment will support those investments. The South-Central Gulf of America helps address the first of those factors and reinforces the other two.

If the goal is to keep the Gulf of America producing at a high level, supporting jobs across the country, strengthening national security, and contributing to US energy supply for decades to come, then maintaining a strong pipeline of future projects is essential. Expanding access to the South-Central Gulf of America is a practical step in that direction.

About the Author

Erik Milito

Erik Milito is the president of the National Ocean Industries Association (NOIA), representing the interests of the offshore oil, gas, wind, carbon capture and ocean mineral industries, among other offshore energy segments. He took on this role in November 2019, bringing more than 20 years of experience in the energy policy sector. Milito is also one of Offshore's 2026 Editorial Advisory Board members.