Review of shallow water GoM structure inventory offers preview of decommissioning requirements

Oil and gas production decline since mid-1980s

Mark J Kaiser

Siddhartha Narra

Center for Energy Studies,

Louisiana State University

The shallow water Gulf of Mexico has witnessed significant changes over the past decade and will continue to be subject to significant changes in the future. Shelf production is not being replenished by drilling and many industry observers believe the GoM shelf is fished out. Dwindling commercial prospects, sustained low oil and gas prices, reduced budgets, operator bankruptcies, and the success of onshore shale development means that drilling and installation activity in the shallow water has been dramatically curtailed in recent years.

Record levels of decommissioning is the result of the maturity of field production and tougher regulatory conditions and oversight.

The purpose of this six-part series is to review structure inventories in the shallow water GoM and provide detailed examinations of producing, idle, and auxiliary structures in the region. The series concludes with decommissioning and installation trends.

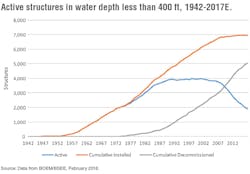

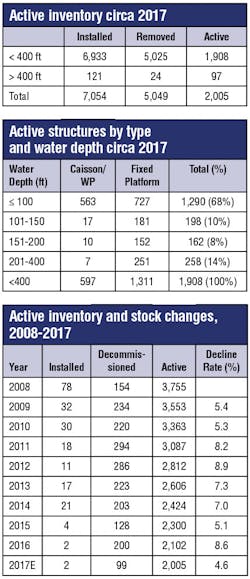

In the first part, the active structure inventory is examined. A total of 7,054 structures have been installed in the GoM since 1947 and 5,049 structures have been decommissioned, leaving an active inventory of 2,005 structures circa 2017.

The number of standing structures in water depth less than 400 ft (122 m) have been cut in half since peaking at 3,974 in 2001. Circa 2017, shallow water standing structures numbered 1,908.

Future installments of the series will cover:

• GoM inventory

• Classification

• Producing structures

• Idle and auxiliary structures

• Decommissioning and installation trends.

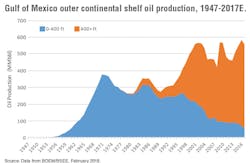

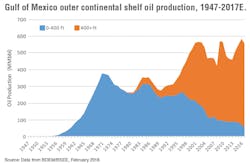

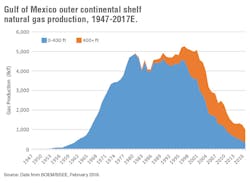

GoM production

According to BOEM data reviewed in February 2018, the GoM produced 557 MMbbl of oil and 1.0 tcf of natural gas through October 2017 and is estimated to have produced 603 MMbbl of oil and 1.17 tcf of natural gas for the year. About 57 MMbbl of oil and 317 bcf of natural gas was produced in water depth <400 ft, representing about 10% of the total oil production and almost one-third of the total gas production in the GoM.

Since 1947, the US outer continental shelf has produced 20.7 Bbbl of oil and 187 tcf of natural gas. More than half of total oil production (12.2 Bbbl) and over 85% of natural gas production have been produced in less than 400 ft water depth, but the region has been in decline since the mid-1980s. Both oil and gas production have fallen steeply on the shelf.

Fortunately, the deepwater GoM is a highly prospective oil province which has supported production in the region compensating for the decline on the shelf. Crude production from 2017 is expected to break the 2016 record level of 585 MMbbl of oil, but gas finds in deepwater have not been significant and total gas production in the GoM continues to fall.

Active inventory

At the end of 2017, there were 2,005 structuresin the GoM associated with oil and gas production. The vast majority of structures reside in water depth less than 400 ft, and circa 2017, there were 1,908 active shallow water structures.

Almost 80% of shallow water structures reside in water depth less than 150 ft (46 m) and over two-thirds of structures reside in less than 100 ft (31 m) water depth. Caissons and well protectors number less than half of fixed platform totals, and fixed platforms represent more than two-thirds of the active inventory circa 2017.

Stock changes

The best single summary graph describing infrastructure trends in the region is the active inventory plot. The dynamics of standing structures can be envisioned using a bathtub analogy, with stock being fed by new installations and depleted through decommissioning.

Active inventory at any point in time represents the difference between the cumulative installed and cumulative decommissioned structure count. The stock change in the active inventory relative to its size characterize its ‘decline rate’ over time. Since 2009, the decline rate of the active inventory has ranged between 5% and 9% per year.

The decline rate of standing structures depends on two independent parameters, installation and decommissioning activity. The difference between these two factors impact inventory size, decreasing if decommissioning activity exceeds installation in a given year, and increasing when installation exceeds decommissioning activity.

Trends

In 1973, the first structure was decommissioned, and in the mid-1980s, removal rates regularly exceeded 100 structures per year and began to attract the attention of both state and federal regulators. However, because the number of installations normally matched or exceeded removal rates, the active inventory remained relatively stable during this time.

For nearly 20 years beginning in the late 1980s, active inventories held steady between 3,800 and 4,000 structures and peaked at 3,974 in 2001. Over the past decade, removal rates have strongly dominated installation activity and standing inventories have declined rapidly.

Installations accumulated at a relatively constant paceup until about 2006 (notice the straight-line nature of the graph) when activity rapidly slowed and decommissioning began dominating activity. Three different periods are apparent, corresponding to the three different slopes in the active curve.

• Before the mid-1980s, decommissioning activity was a relatively minor affair with activity levels averaging less than 30 structures per year.

• From the mid-1980s through 2006, cumulative removals approximately track cumulative installations, and the two graphs roughly parallel each other and the number of active structures were in relative equilibrium.

• Since 2008, installation activity has slowed down considerably while decommissioning has accelerated, causing the active inventory to drop in a fashion that mimics its rise in the 1970s.

From 1987-2006, there were on average 134 structures installed per year and 122 structures removed. From 2007-2017, there were on average 26 structures installed and 198 structures decommissioned.