Is the offshore cup half full or half empty?

Maybe we should start this conversation by first acknowledging our collective behavior as risk takers and optimists if we have worked in the oil and gas industry for any reasonable amount of time. In December 2019, we were “enjoying” a return to WTI at $60/bbl, a long hard journey from the $30/bbl toward the end of 2015. There were good reasons for optimism going into 2020. How could we have known then what was to happen a few months later? Was not our logic sound given the information available to us at the time?

In any case, we are now recovering from both oversupply and COVID impacts. Depending on the human toll and economic damage done by further COVID-19 waves, supply and demand appear heading back to 2019 levels by 2022-2023, with a return to $50-70/bbl for WTI. Note that IEA have set a range of 2022-2025 for demand returning to 100 MMb/d. The IEA Delayed Recovery Scenario assumes a prolonged pandemic and deeper economic slump conspire to delay return to 100 MMb/d demand until 2025. Prices, if sustained at or above $50/bbl for WTI, should bring a return to 2019 activity levels offshore. Read on if you want to believe but are not yet fully convinced. The cup is nearing half full and continuing to fill as you read this.

Commodity pricing

Until the COVID-19 induced drop in 2020, oil prices for the past 15 years have remained between $50 and $80/bbl, excepting brief but unsustainable spikes in 2007 and 2013. A drop from $120/bbl in 2013 to $50/bbl in 2016 led to a significant reduction in offshore final investment decisions (FIDs). Since that recalibration in 2016, commodity prices within the $50-$80/bbl range have supported a steady year over year increase in offshore FIDs until 2020.

Supply and demand

Due to finite storage capacity, supply and demand cannot remain out of synch for any length of time without a dramatic and unsustainable impact on price. If you do not believe that hypothesis, take a look back when the price for WTI was briefly negative in 2Q 2020. Supply and demand for oil have been steadily marching from 55 MMb/d in 1985 to 100 MMb/d in 2019, at a rate averaging 3% per annum.

Project sanctions

Project sanctions or FIDs for offshore fields were recovering from a low of 38 in 2016 to a high of 104 in 2019. Those FIDS represented $23 and $96 billion in capital spending respectively. FIDs in 2020 fell to 19 as operators slashed their capital spending plans. The outlook from Rystad Energy is favorable going forward, with expectations for 60 FIDs in 2021 and 147 in 2022, or $60 and $118 billion respectively. Given the reductions of headcount and bankruptcy filings in 2020, one might have reason to question whether human and financial capital could become constraints for that level of activity in the near term.

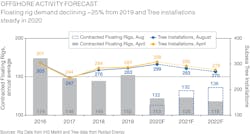

Offshore services

Spending on services has been hit particularly hard in 2020 as operators focused on cash preservation. Some facts:

- Drilling utilization is relatively flat, albeit at a lower population of rigs given the attrition over the past five years.

- Expected offshore spend is relatively flat.

- Offshore projects are often slow to start, relatively large in scope and tend to continue through to completion once started. This behaves somewhat like a shock absorber when it comes to maintaining a steady flow of project activity offshore as compared to onshore projects which are quicker to start, often smaller in scale and have higher rates of depletion.

Floating production systems

Deepwater developments continue to command the largest amount of capital expenditures, compared to shallow water and shelf activities. This is good news to those contractors with a deepwater focus, be it through subsea wells or floating production systems. FPS awards were growing steadily from nine in 2016 to 18 in 2019 until falling off the cliff to four in 2020. With the forecast for deepwater FIDs growing beyond 2019 levels, expectations for FPS should follow suit. Once again, the same short-term constraints of human and financial capital could also apply.

Bright spots

Okay, so maybe you still want to believe in a relatively near-term recovery, but you need some specifics to hang your hat on. A virtual journey around the world may prove beneficial. This journey, so to speak, begins in Brazil. The country’s presalt production reached 2.2 MMb/d in 2020, and is expected to reach 5 MMb/d by 2030. The Búzios and Mero fields alone have combined recoverable reserves of approximately 15 Bboe. Current plans for these fields include the installation of 10 new FPSOs by 2030, each having crude oil processing capacity of 180,000 b/d or more.

Still in South America, but further up the East coast, are Guyana and Suriname. According to a US Geological Service study released in 2012, the Guyana-Suriname basin is estimated to contain 13.5 Bboe of undiscovered oil. Exxon announced its Liza 1 discovery in 2015 with estimated reserves of 2.5 Bboe. Liza 1 production began in December 2019. In subsequent discoveries with its various partners, Exxon has announced total recoverable reserves of 8 Bboe and production forecast at 750,000 b/d by 2025. Rystad Energy predicts that Guyana production could reach 1.2 MMb/d by 2030.

The Tamar and Leviathan discoveries by Noble Energy and the even larger discovery of Zohr by Eni have turned the Eastern Mediterranean into a hotspot for gas, with Egypt having LNG infrastructure to facilitate export. Very likely this will unleash further exploration and production in this energy rich region.

As a reminder, this conversation is about the outlook for oil and gas in general and more specifically offshore. However, there is a growing interest in the potential for incremental energy supply, particularly from renewables, which is also a bright spot for the offshore industry. Much of the renewable energy growth is forecast to come from offshore wind. Since our industry has the knowledge, skills and abilities to design, fabricate and install facilities offshore, renewables represent an adjacent space that many operators and oilfield service companies have and will continue to pursue. While starting from a smaller base, renewables are forecast to have the greatest rate of growth over the next 30 years.

The pivot

“The Pivot” is a term we use to describe the environment in which the world’s economies move toward a reduction in greenhouse gas emissions, with the subsequent need to consume lower carbon fuels. Many of the major operators have made and are making commitments toward a net zero position in their carbon footprint by 2050. Now before you run for the exit in your oil and gas career or divest your oil and gas investments, here are a few points to consider:

1. Oil production is forecast to remain at current levels, in absolute amounts, for at least the next 20 years, albeit it will account for a smaller percentage of a growing energy market.

2. Natural gas production is forecast to grow by 6-7% per annum over the next 20 years as a lower carbon intensity fuel.

3. Many of the operators are planning to invest in, own, and operate offshore wind energy facilities in a significant way.

4. Carbon capture and other sources of renewable energy are also being developed. This will represent significant additional investment for the major operators and new players. Endeavor is working in this space with our clients.

5. As with oil and gas, the renewables market will also have to show that it can obtain approvals in a timely manner; and respond and adapt to new and potentially disruptive technologies. These challenges, and the need for governmental incentives, have the potential to delay growth in the renewables market.

Conclusions

Since 2014-2015, the offshore industry has seen multiple bankruptcies, significant personnel reductions, and marginal or negative earnings. In 2019, the market appeared ready for recovery, but those hopes were dashed by COVID-19 and low oil prices in the year that followed. But the recovery was not eliminated, it was just pushed out a few years. A recovery from COVID-19 will set the stage for economic recovery and growing energy demand. If you can hold on, our industry will yet again rise from the ashes and provide significant opportunities for companies, investors, and employees alike.