GLOBAL DATA

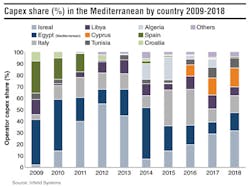

This month, Infield Systems examines offshore capex in the Mediterranean Sea area. Investment in the deep and ultra-deepwater Levant basin, a gas-rich frontier in the eastern Mediterranean, is forecast to see capital investment from Israel, Cyprus, and Egypt, and is expected to see the highest spend. Elsewhere, investment is expected to be focused primarily on the traditional areas of the Italian Adriatic Sea, the Tunisian Gulf of Hammamet, and the Libyan Gulf of Sirte.

The Mediterranean has never been the most prolific production basin in the world. However, capex relating to deep and ultra-deepwater developments in this region is expected to ramp up throughout the forecast period. Ultra-deepwater fields are expected to account for 35% of Mediterranean capex at the end of the forecast. The Levant basin forms the greater part of this and with increasing interest in targeting gas developments globally, the Levant basin is expected to see significant levels of investment continue.

Israel is expected to account for the highest capex in the region. The Tamar Phase 2, Leviathan, and Dolphin developments are expected to drive expenditure over the forecast. Cumulatively, these projects represent 13% of total Mediterranean capex. Egypt was historically the largest investor in the region. Despite falling behind Israel in the forecast period, it is still expected to see capex on a large number of small developments. The Raven development, at 3% of overall capex, is the largest of these developments in the Egyptian Mediterranean, targeting 4 tcf of gas. Italy, historically one of the larger oil and gas producers in Europe, saw relatively low levels of investment over the historic period. Infield Systems expects to see a resurgence in Italian capex with the Cassiopea and Prezioso fields seeing high levels of investment and the Triton Adriatic FSRU expected to go ahead toward the end of the timeframe. Libya and Tunisia are expected to see large amounts of investment on the Bahr Essalam and Zarat developments, respectively. Cyprus, with the Aphrodite field in the Levant basin, is expected to see capex pick up in the last few years of the forecast.

− Kieran O'Brien, Energy Researcher, Infield Systems Ltd