FLNG market thrives amidst projects boom

Editor's note: This feature first appeared in the March-April 2024 issue of Offshore magazine. Click here to view the full issue.

By Bruce Beaubouef, Managing Editor

The global FLNG market is revving up, spurred on by lower unit costs, standardized designs, and growing demand for quick-to-market LNG supply. A report issued by Wood Mackenzie last fall indicated that 8.5 million tonnes per annum (mmtpa) of FLNG capacity had been sanctioned in 2022, and that as of August 2023 there was 10.0 mmtpa of FLNG projects were under construction. This surge in market interest, the firm commented, made it clear that investor interest has returned to the global FLNG market after several years in the project doldrums.

“By 2026, almost 22 mmtpa of floating supply will be operational,” said Fraser Carson, Senior Gas Research Analyst at Wood Mackenzie. “With international oil companies, upstream producers and midstream specialists all moving projects towards final investment decisions [this] could push capacity even higher by 2030.”

The report added that lessons have been learned from the FLNG sector’s chequered history with issues around cost overruns, project delays and reliability all seeing major improvements over the last few years. Recent FLNG projects have met their construction schedules. Coral FLNG, which shipped its first cargo in November 2022, was successfully delivered on time and on budget. Similarly, the Gimi FLNG unit experienced minimal delays during its construction and arrived at site in offshore Mauritania/Senegal in February this year.

Plus, new fast-to-market LNG supply is more valuable than ever. Europe has rapidly shifted away from piped Russian gas, and towards the global LNG market, intensifying competition for the limited supply that is available. There is limited near-term supply growth. And with onshore LNG taking an average of four years to develop, demand is strong for new projects that can be brought online quickly.

In addition, FLNG has become cost-competitive with other field development options. The generally lower capital costs associated with FLNG are attractive to investors. With standardized designs, indicative costs for the FLNG unit can be derived, says Wood Mackenzie. Golar’s conversion designs, such as the MkII Gimi for Tortue Phase 1, can be as low as US$550/tonne, while Samsung Heavy Industries’ and Wison Offshore & Marine’s newbuild orders for ZLNG and Marine XII are both around US$800/tonne. This compares favorably to onshore LNG plant capex, which is currently around US$950/tonne for US Gulf Coast projects, according to Wood Mackenzie.

Another point in favor of FLNG designs are their increased accessibility by producers and developers. The initial, challenging experiences of FLNG project development have generated strong demand for a simplified approach. Shipbuilders like Wison and Samsung now offer standardized newbuild FLNG designs, available for a range of production and storage capacities. Golar offers three standard FLNG designs, two conversions and one newbuild option. New Fortress Energy is developing the liquefaction modules for its Fast LNG designs with a fixed capacity that can be scaled up.

“After a stuttering start, FLNG is proving to be a reliable commercialization option,” Carson said. “The utilization of FLNG facilities in Cameroon and Mozambique has been strong over the 18 months, with the units producing at close to or above 100% of available capacity.”

African FLNG projects

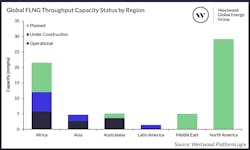

Africa has been at the epicenter of FLNG momentum. That continent should account for 56% (10.2 mmpta) of capacity onstream during the 2023-27 period, says Westwood Global Energy Group. In recent years, resource-rich African markets have faced challenges developing gas for export, including from armed insurgency and infrastructure sabotage. FLNG is removed from these above-ground risks. It also provides African producers with an alternative to supplying the domestic market. Use of FLNG units to develop large gas reserves offshore Mauritania, Senegal, Tanzania and Mozambique is also seen as a lesser security risk to IOCs than local onshore alternatives.

Over the past year, experienced FLNG developers Eni and Perenco have sanctioned a two-phase floating development in Congo and a barge-based project in Gabon, respectively. But new entrants, such as UTM offshore and NNPC, are also considering FLNG to develop Nigeria’s stranded offshore volumes. In East Africa, FLNG continues to be linked as a potential development option for the Rovuma partners.

Other African FLNG projects set to be sanctioned in the coming years likely include a second unit at Eni’s Area 4 development offshore Mozambique and other(s) for bp’s Yakaar-Teranga and BirAllah gas discoveries offshore Senegal and Mauritania.

Meanwhile, other African FLNG projects have recently started production operations, or will do so soon. The FLNG Gimi vessel has reached the Greater Tortue Ahmeyim (GTA) field location offshore Mauritania and Senegal following a voyage from the Seatrium conversion yard in Singapore. Upon completion of preparatory activities, the vessel will be directed to its berth at the projects’ hub for subsequent connection to the offshore gas pipeline. The vessel is due to operate on the GTA field for the next 20 years.

Elsewhere, Eni has introduced first gas to the Tango FLNG vessel moored offshore Congo, 12 months after taking FID on the Congo LNG project. On completion of the commissioning phase, the vessel will produce its first LNG cargo sometime within 1Q 2024.

Tango FLNG has a liquefaction capacity of close to 1 bcm/yr and is moored alongside the Excalibur floating storage unit via a split mooring configuration. Congo LNG will monetize gas resources from the Marine XII permit and reach around 4.5 bcm/yr of plateau gas liquefaction capacity under a phased development, with a target of zero routine gas flaring. A second FLNG facility (3.5 bcm/r capacity) is under construction and should start production for Eni in 2025.

Still elsewhere, Wison New Energies says that it has started the design validation and early engineering studies for two FLNG projects owned by Nigerian companies Ace Gas and FLNG and Transoceanic Gas & Power. In January, Wison reported that it had launched the pre-FEED phase for two 3 million tons per annum (mtpa) FLNG vessels under a “design one and build two” strategy. Transoceanic’s FLNG project is located offshore Pennington and proximal to OML 289, a block operated by the company on behalf of Cleanwaters consortium. It is designed to supply 3 mtpa of LNG to the international market, and 150,000 metric tons per year (MT/yr) of LPG to the domestic market. As part of the phased development plan, the project will deploy a floating power barge concept, starting with a Phase 1 Power capacity of 250MW.

The Ace Gas and FLNG project is located offshore Escravos and is also designed to supply 3 mtpa of LNG to the international market, and 150,000 MT/yr of LPG to the domestic market.

Offshore Asia

In Asia, the Madura FLNG project seems to be moving forward as part of the development of the Madura gas field offshore Indonesia. Last fall, Bumi Armada signed a provisional agreement concerning the Madura gas field and others in the area with PT Pertamina International Shipping (PIS), the logistics subsidiary of Indonesia’s state energy company Pertamina, and gas trading company PT Davenergy Mulia Perkasa. The agreement could lead to Bumi Armada and PIS collaborating on the design, engineering, construction and installation of an FLNG unit at the field in the Madura Strait, and an LNG carrier to transport LNG to other users.

Upcoming FIDs

Several FLNG units are expected to be sanctioned this year according to Westwood, which estimates that the FLNG market has an expected EPC award value of approximately $15 billion.

One of these is the Cedar FLNG project offshore Canada, which seems to be moving forward. Samsung Heavy Industries (SHI) recently announced the award for a newbuild FLNG unit valued at $1.5 billion, believed to be for the Cedar FLNG vessel. That announcement had been preceded by another one in December by Black & Veatch, which said that it had signed a heads of agreement (HOA) with Cedar LNG Partners LP and Samsung Heavy Industries (SHI) to secure capacity in SHI’s shipyard to support Cedar LNG’s targeted commercial startup in Kitimat, British Columbia. The HOA also calls for the stakeholders to work together to exclusively advance the EPC agreement for the proposed FLNG facility. According to Black & Veatch, this export facility will employ a near-shore FLNG vessel utilizing its PRICO liquefaction technology integrated with the hull and LNG storage tanks. Black & Veatch also says that it will be responsible for complete topside design and equipment supply. An FID on the Cedar FLNG project is expected soon.

Other FLNG units that may get the FID this year include Delfin Midstream’s FLNG project off the coast of Louisiana; Nisga’a Nation’s Ksi Lisims FLNG project (Canada); Genting Oil and Gas’ AKM FLNG unit (Indonesia); Eni’s Coral Norte unit (Mozambique); and UTM Offshore’s Yoho FLNG project (Nigeria).

The Delfin LNG Deepwater Port project, which calls for four FLNG units offshore Louisiana, is apparently unaffected by President Biden’s recent pause on LNG exports, having its approvals in place already. To advance the project, last fall Delfin Midstream Inc. entered into a design and engineering contract with Wison Offshore & Marine to build new FLNG vessels for the project, and thereby accelerate the development of the remaining FLNG vessel slots at the proposed deepwater port. The Delfin LNG Deepwater Port will be designed to export up to 13.3 million tons of LNG per annum. Delfin says that it has secured commercial agreements for LNG sales and liquefaction services, and is in the final phase towards FID on its first two FLNG vessels.

FLNG challenges

But for all its advantages, FLNG is not without its challenges. A simple, fast-to-market solution is the fundamental appeal of FLNG, but it may not be a practical option for every remote field development scenario. The requirements for gas processing or difficult metocean conditions can quickly add complexity and increase costs.

Regional conflict and related uncertainty can also undermine projects. One example is the Leviathan FLNG project offshore Israel, which until recently had seemed to be moving forward. NewMed Energy and Chevron had previously confirmed Leviathan FLNG’s design concept and had hoped to issue the FID on the project this year. But a report issued last November cast doubt upon the project due to its rising costs. And more recently, the decision by ADNOC and bp to delay a proposed $2-billion purchase of NewMed Energy – apparently in response to the conflict in Gaza – will likely have a chilling effect on the project.

Bullish outlook

“Despite the bullish outlook, FLNG is not without risks,” Carson conceded. “Still, we estimate that up to 20 mmtpa of new FLNG capacity will be sanctioned over the next two years and this will primarily be developed in markets where there are concerns of cost blowouts, scheduling delays and security risks.”

About the Author

Bruce Beaubouef

Senior Lead Reporter / Managing Editor

Bruce Beaubouef is Managing Editor for Offshore magazine. In that capacity, he plans and oversees content for the magazine; writes features on technologies and trends for the magazine; writes news updates for the website; creates and moderates topical webinars; and creates videos that focus on offshore oil and gas and renewable energies. Beaubouef has been in the oil and gas trade media for 25 years, starting out as Editor of Hart’s Pipeline Digest in 1998. From there, he went on to serve as Associate Editor for Pipe Line and Gas Industry for Gulf Publishing for four years before rejoining Hart Publications as Editor of PipeLine and Gas Technology in 2003. He joined Offshore magazine as Managing Editor in 2010, at that time owned by PennWell Corp. Beaubouef earned his Ph.D. at the University of Houston in 1997, and his dissertation was published in book form by Texas A&M University Press in September 2007 as The Strategic Petroleum Reserve: U.S. Energy Security and Oil Politics, 1975-2005.