Choppy waters ahead for offshore industry

Lesley G. Mitchell • Robin C. Mann

Deloitte

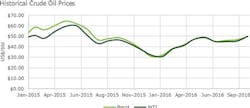

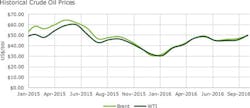

As 2017 begins, the main change in the market from the start of last year regarding oil prices is that the Organization of the Petroleum Exporting Countries (OPEC) has come to an agreement to curb supply. This may bolster the short-term outlook for the oil industry, but the long-term impact remains to be seen. Prices were volatile over the last year, with lows of $30/bbl for WTI and highs of just over $50/bbl. This is likely to continue, as there is concern whether all OPEC countries will adhere to the agreement and whether non-OPEC countries will fill the gap quickly and the oversupply returns. The impact to the offshore industry may not be substantial as the long-term nature of projects does not lend to being nimble. However, early 2017 cash flows could be strengthened by the market reaction to the agreement.

An oil oversupply is being carried into the new year, although the International Energy Agency predicts this could be worked through the system by late 2017. This potentially good news is tempered by the fact that similar forecasts for the past two years about the oversupply dissipating have not transpired. Industry continues to find efficient ways to deploy moderate capital and offset any production declines that would have been expected by now.

In the world of offshore exploration and development, activity remained relatively flat over the past year as producers attempted to either weather the storm or adjust to the new reality. However, things are not the same in all offshore areas. Some regions have shown interesting dynamics as companies adjust, which could have positive indications for future activity. The outlook for these regions is summarized below.

North Sea

The North Sea is a highly developed jurisdiction that has entered a phase of super maturity. Declines in drilling rates did not decrease production from this region in 2015 or 2016. Drilling dropped in October 2016 when Norway almost halved the number of rigs, from 16 to nine, from the previous month. However, a recent announcement by major oil companies to move ahead with developing the Oda field gives some hope for a rebound in this region in the coming years.

Middle East

Offshore drilling for the Middle East has not changed significantly over the past year, though activity has increased in many countries since the price dropped. Saudi Arabia and UAE are all drilling at near record rates (70% of the activity in the region), which some argue is a move to position themselves to be able fill the gaps in supply due to big projects in other regions being cancelled. That claim assumes that the shale plays in the US will not be able to fill the gap, which is a bullish assumption. There have also been reports that Saudi Arabia’s capital budget has been cut to around 30% of its 2015 budget, which would take a toll on the activity that can be maintained in this region.

Gulf of Mexico

Offshore drilling in the US has been relatively steady over the past year. The Mexico component has decreased throughout 2016, falling from a 50% share of drilling in the Gulf of Mexico to 40%. Fewer shallow-water permits were issued for the Gulf of Mexico, while deepwater permits held relatively steady, indicating that any future activity in this region is going to be driven by deepwater prospects. The costs associated with exploring in deepwater are significant, so the hope is that prices will continue to rebound during these longer-term projects.

Asia/Pacific

In March 2016, the Indian government released a price formula for undeveloped fields; this has led to a renewed interest in shelved projects. All undeveloped offshore projects receive a higher price than the previous formula provided, with deepwater projects receiving the most benefit. However, the prices to be received using this new formula decreased during the course of 2016 due to the last four redeterminations. On the positive side, one of India’s largest producers has continued its investment despite the challenging prices over the past two years.

Expectations for 2017

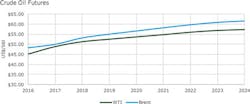

Oil prices are expected to gain momentum through 2017 with the OPEC agreement. However, the onshore industry is poised to bring on production quicker and at a lower cost than the offshore industry, making it extremely difficult for offshore fields to fill any significant supply gap. As the demand outlook softens, many forecasters predict oil prices will come down in the long term. Only the most cost-effective projects are likely to continue, with the most prolific projects in low-cost regions likely to be sanctioned.

Current prices are causing earlier-than-anticipated problems for companies that are decommissioning. The low prices have accelerated the timeframe in which such activities must occur at the same time the industry is grappling with higher standards for decommissioning, which are expected to drive costs higher than originally forecast. Companies will have to factor these expenses into their budgets, which will detract from the ability to explore and grow effectively. Therefore, capital budgets are expected to be strained through 2017.

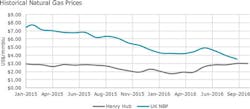

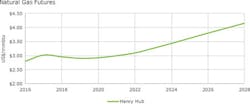

Meanwhile, natural gas prices are expected to have marginal growth over 2017. Offshore activity targeting natural gas is minimal in the US. In October 2016, for example, only 4% of all rigs focused on natural gas. Internationally, 20% of rigs targeted natural gas during the same month, with India and Thailand being the major drivers of activity.